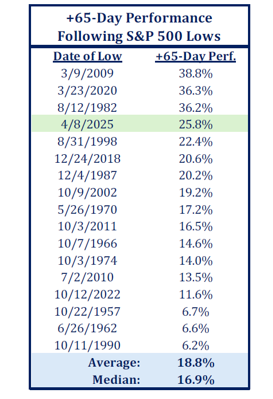

Given perfect foresight into the events of the second quarter-Liberation Day, a U.S. debt downgrade, a collapse in consumer confidence, bunker busters dropping over Iran-many investors would have sat it out. Remarkably, after starting April with a historic selloff, global equities ended the quarter at or near record highs. As of this writing, the S&P 500 is up roughly 26% from the April 8th low-the 4th best rally in the first 65 trading days off a major market bottom ever. Additionally, the index also staged its quickest recovery to an all-time high after a decline of greater than 15%. Investor sentiment shifted quickly from fear to the fear of missing out (FOMO).

During our webinar on April 14th, we reviewed several potential catalysts that could stabilize markets and discussed other tailwinds that might develop as the year progressed. Admittedly, we did not know for sure if or when they might occur, but gladly several of them did, leading to a strong rebound in risk assets.

Trade Policy: A more moderate approach

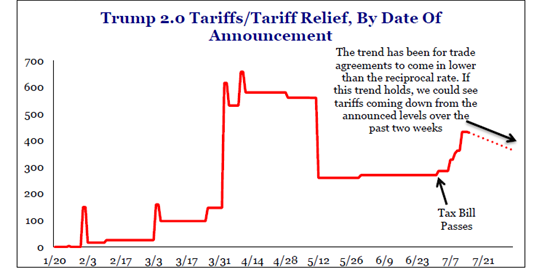

The tariffs proposed on Liberation Day, combined with what had previously been proposed or implemented, amounted to approximately $620bn (ultimately closer to $700bn). At 2% of GDP and an effective tariff rate of over 20%, these measures very likely could have caused a global recession. The reduction in proposed tariffs to a still high (but manageable) $270bn was a hugely positive development for markets. Furthermore, we believe the decline of Peter Navarro and the ascendancy of Treasury Secretary Scott Bessent in both policy and negotiations was significant. Bessent is an experienced investor who understands markets and the ramifications of policy on markets. We are not completely out of the woods yet as trade narratives and headlines continue to shift. Nonetheless, despite a less than elegant start to his second term, we still believe Trump is a deal-focused, transactional President.

Economic Data: Better than feared

The collapse in “soft” data earlier this year caused concern about an imminent decline in consumer spending and the labor market. Despite great uncertainty and the looming effects of tariffs, consumption has remained resilient. While some of this resilience can be attributed to tariff front-running on goods, real-time high frequency services spending data (e.g. dining, lodging, travel) has also remained firm. However, we have observed a more mixed set of data over the last few weeks.

The U.S Corporate Earnings: Surpassed expectations

First quarter year-over-year earnings growth significantly outpaced expectations. The April 1st estimate was 8% with actual earnings growth coming in closer to 14%. Technology and communications services companies again carried the load, but there were also good results from financial and industrial companies suggesting profit growth is broadening. While still early, the second quarter earnings season has started off strong with solid reports from the likes of Goldman Sachs, Johnson and Johnson, and GE Aerospace.

Sequencing of Policy: “Less spinach, more ice cream”

In our March 6th market update, we borrowed a phrase from one of our research providers that we felt aptly described the sequencing of policy during Trump 2.0-“mostly spinach now, ice cream later.” This sequencing contrasts with Trump 1.0 which began with pro-growth, pro-market policies in 2017 and pivoted to tariffs in 2018.

We pointed out that later in the year we would likely see an extension of tax cuts, potential new tax cuts, and ongoing tailwinds from deregulation and lower energy prices.

Importantly, the OBBBA (One Big Beautiful Bill Act) may mitigate the effects of tariffs. The Congressional Budget Office estimates the Act could stimulate GDP growth by close to 1% next year while the Yale Budget Lab estimates trade policy will lower growth by between 0.5-1.0% this year. The bill contains several measures that could underpin business investment and economic growth:

Deregulation in the banking sector should free up excess capital and increase lending activity. Stablecoin legislation may increase Treasury Bill demand, potentially offsetting concerns related to issuance.

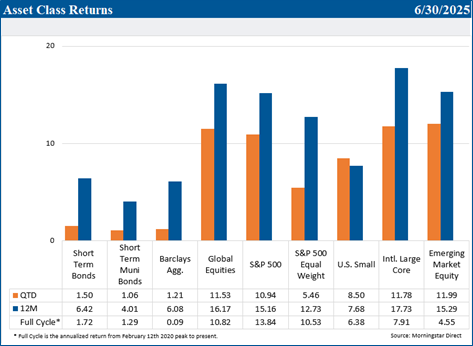

Your globally diversified equity portfolio benefitted from the continued strong performance of international developed and emerging market stocks. A weaker U.S. dollar certainly helped. The 10% decline in the U.S. dollar index was the weakest first half performance since 1973. Additionally, investors remained optimistic about improved prospects for economic and corporate earnings growth overseas, as well as meaningful and targeted fiscal stimulus, particularly in Europe. China, mired in sluggish growth and still fighting deflation, may finally be embracing the idea that spurring domestic consumption is the best approach to sustainably improve economic growth.

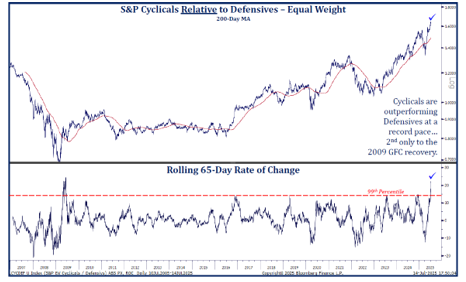

In the U.S., technology stocks reasserted their leadership as the quarter progressed. More cyclical (economically sensitive) sectors such as financial and industrial stocks also rallied sharply. The relative performance of cyclical to defensive sectors reached a new high. In fact, cyclicals are outperforming defensives at the fastest pace since the post-Great Financial Crisis recovery. This is typically not the behavior you see if the market is expecting economic malaise.

Bonds and diversifying assets rose modestly during the quarter. After spiking in early April, Treasury market volatility settled down. The curve continued to steepen. Similarly, credit spreads (an important market barometer we have discussed in past commentaries), ended the quarter at historically tight levels after rising sharply during the post-Liberation Day turmoil. While a July interest rate cut is likely off the table, recent commentary from Fed officials suggest September is a “live” meeting. The Federal Reserve remains in a wait and see mode as they assess the potential impact of tariffs on inflation.

We expect the U.S. economy to muddle through the remainder of the year before potentially accelerating next year as trade, fiscal, and monetary policy become more supportive of growth.

As always, our eyes are on the labor market and the U.S. consumer. Small business hiring intentions suggest a downshift to a 50k-100k pace over the coming months. This pace would likely cause the unemployment rate to drift towards or past 4.5%, prompting the Fed to ease. Furthermore, we noted earlier that recent consumer spending data has become more mixed. Real consumption may slow to a 1% pace during the second half of the year.

Tension between the Trump administration and Federal Reserve Chairman Jerome Powell may be an underappreciated risk. While seemingly a sideshow a couple of months ago with Trump ultimately softening his comments towards Powell, the administration has recently upped the ante. Trump may be using the Fed’s management of renovating its headquarters to either fire Powell or create a sufficiently uncomfortable environment that Powell ultimately decides it’s not worth sitting out his term. The former approach would be politically unpopular, legally challenging, and market unfriendly. The latter tactic may persist. Furthermore, announcing Powell’s successor well in advance of the end of his term may create volatility in the bond market if the “shadow” Fed chair communicates his or her policy outlook.

Is the recent outperformance of international equities the start of a sustainable, long-term trend? While we do not believe in the imminent demise of U.S. exceptionalism, we assign a higher probability of more competitive ex-U.S. equity returns going forward. International equities may now have several catalysts to gradually narrow the large valuation discount that has developed over the last 15 years.

Bond yields are historically attractive, and your fixed income portfolio will continue to produce steady, monthly income. Diversifying Assets should continue to provide uncorrelated return streams.

In the second quarter, we increased your allocation to an equity mutual fund that invests in large-cap, high quality U.S. and developed international companies. During the third quarter, and for most clients, we will slightly reduce your fixed income allocation and reinvest that capital into a new diversifying assets strategy. The fund satisfies our three primary requirements for a diversifying asset-low correlation to both stocks and bonds, a return expectation between the two asset classes, and a low correlation to the other funds in your diversifying asset portfolio. Additionally, we anticipate the fund to provide steady, monthly income. More information to follow in future communications!

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,