Tue, April 15, 2025

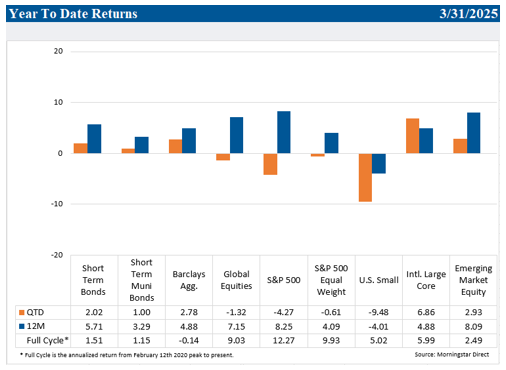

Diversification proved to be valuable during the first quarter. Despite the barrage of negative headlines and heightened volatility, a well-balanced, multi-asset class portfolio finished the quarter relatively unscathed.

U.S. equities declined during the quarter led by weakness in mega-cap technology stocks (the Mag 7). Conversely, a weak U.S. dollar, prospects for improved relative economic and earnings growth, and the potential for a transition from fiscal austerity to stimulus led developed international stocks to deliver strong returns. In fact, the month of March saw one of the largest relative performance gaps ever between the U.S. and developed international stocks. Emerging market equities also advanced. Fixed income returns were positive as yields declined in the face of growth concerns in the U.S. As a group, diversifying assets (low correlations) rose slightly.

While volatility increased in the first quarter, it was no comparison to what we experienced in the first two weeks of April. The recent volatility in both U.S. stocks and bonds has been historic, rivaling past periods of crises since World War II.

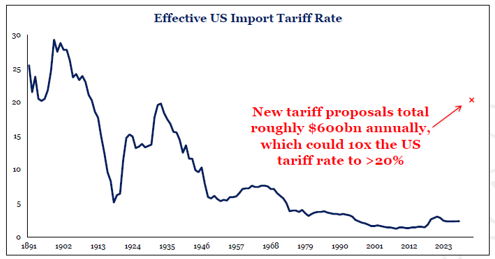

The size and scope of President Trump’s tariff proposals on April 2nd far exceeded investors’ expectations, including some of the most bearish forecasts. At just over $600 billion, the proposed tariffs would equate to roughly 2% of U.S. Gross Domestic Product (GDP), increase the effective U.S. import tariff rate from 2% to over 20%, and represent the largest tax hike in the modern era. Understandably, markets were stunned.

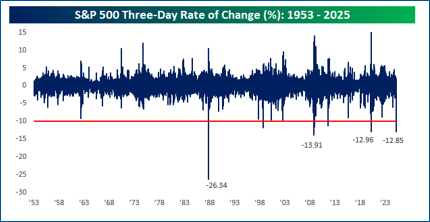

The S&P 500 fell over 12% between Thursday, April 3rd and its intra-day low on Monday, April 7th. This was only the fourth time since World War II that the index declined by that amount in such a short period of time. The other three occurrences were during the crash of 1987, the Great Financial Crisis in 2008, and the Covid pandemic in 2020.

However, when Trump announced a 90-day reprieve on reciprocal tariffs on Wednesday, April 9th, the S&P 500 surged 9.5%, the third largest daily return since 1950. This was a helpful reminder that volatility can work both ways. According to JP Morgan Asset Management, over the last 20 years seven of the market’s ten best days occurred within two weeks of the ten worst days.

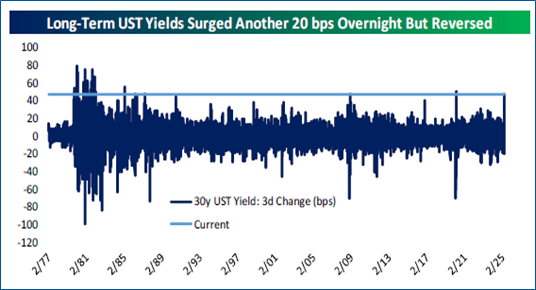

Perhaps the most important developments occurred in the bond market. In the immediate aftermath of Liberation Day, U.S. Treasury bonds acted as traditional safe havens. Investor concerns about economic growth drove bond prices higher and yields lower. The 10-year Treasury yield reached its lowest level since last fall. However, yields quickly reversed. The 10-year yield rose from 4.0% to 4.5% in a matter of days while the 30-year yield recorded its biggest three-day jump since 1982. Theories abound as to why this reversal happened. It likely represents a confluence of factors: fundamental and technical. Central banks or sovereign wealth funds may have played a role. However, the severity of the move suggests forced liquidations, likely deleveraging from hedge funds or other investment strategies who either had to meet margin calls or were caught on the wrong side of highly levered trades.

Moreover, credit spreads widened significantly, particularly high yield bond spreads. A credit spread is the difference between the yield on a treasury bond and the yield on a corporate bond of the same maturity. When that gap widens, it means investors are requiring a higher yield to compensate them for the risk of holding the bond, either due to concerns about the economy, corporate earnings, liquidity, or general financial conditions. We track spreads closely as they are an excellent barometer for the bond market’s assessment of various risks.

We believe the developing stress in the bond market is what ultimately led Trump to declare the 90-day reprieve on reciprocal tariffs (excluding China). Once market volatility begins to affect the bond market, a response has typically followed. The Covid pandemic is the most recent example, but there were several others going back as far as 1958. Treasury Secretary Scott Bessent has openly discussed the importance of the 10-year Treasury yield, and as an experienced investor is keenly aware of the importance of both the treasury and credit markets. The 90-day reprieve is also a reminder that, despite the seemingly unconstrained approach of the administration, there may indeed be constraints. This could have ramifications for future trade and fiscal policy.

Economic and Market Implications

While the reprieve on tariffs may have temporarily removed the worst-case scenario, considerable uncertainty exists regarding the timing, level, and scope of tariffs. Additionally, ongoing workforce reductions in the government, funding cuts, and deportations are also increasing uncertainty and lowering consumer and business confidence.

In our communication to you in early March, we discussed how the sharp decline in confidence was the impetus for an economic growth scare, a sudden fear that economic growth will weaken or decline.

We reviewed growth scares in the context of history-citing 2015, 2018, and 2022 as recent examples in which markets fell sharply (between 15-25%) only to stabilize, and reverse course as growth stabilized. In 2022, we experienced a technical recession (two quarters of negative GDP growth) but avoided a broader downturn that affected employment and spending.

Therein lies the key question – will this slowdown morph into a recession? As we surmised in that communication, the risks of recession are rising and may still be. Economic forecasting is often difficult, and perhaps even more so in the current environment. Nonetheless, our eyes are on the U.S. consumer and the labor market.

Consumer Spending

Consumer spending comprises approximately 70% of U.S. GDP. It’s hard to avoid a recession if there’s a significant downturn in consumption. After a robust fourth quarter in which real consumption growth increased 4.0%, the pace may have slowed to less than 1.0% in the first quarter. The March headline retail sales number was strong, but the data should be taken with a grain of salt as it undoubtedly reflects a surge in goods purchases (especially autos) ahead of tariffs.

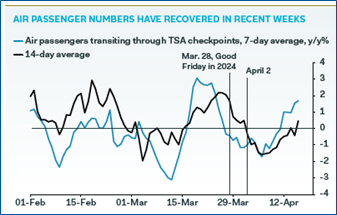

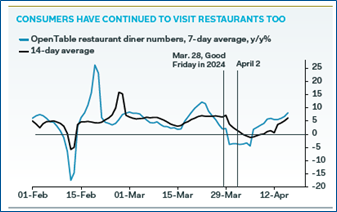

Still, recent high frequency spending data do not yet suggest a significant retrenchment. Open Table dining reservations have been growing at a brisk 5% pace since April 2nd. Data from STR Global shows that hotel occupancy rates are in-line with seasonal norms. Moreover, the Visa U.S. Spending Momentum Index, a measure of actual aggregate spending behavior by millions of consumers, held up well in February and March. Air passenger numbers have recovered recently. Thus far the “soft” data (surveys) and the “hard” data (actual spending) have not converged.

Labor Market

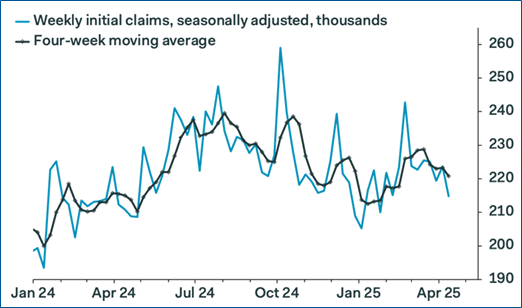

The labor market slowed in January and February but bounced back in March with nonfarm payrolls rising 228,000. For the last several months, the labor market has exhibited a pattern of “less hiring, but little firing.” How this dynamic evolves over the next several months is key. Small business hiring intentions have cooled but are still positive, while layoffs ex-government have remained benign. Weekly jobless claims have also been surprisingly tame. The Gig economy may be providing an offset; the number of multiple job holders reached a multi-month high. However, this is not sustainable. Economists we follow suggest the unemployment rate will reach 4.5% this year with estimates as high as 5.0%. If unemployment reaches 4.5%, we believe the Federal Reserve will begin cutting interest rates.

A recession is not inevitable, but the risks are rising. While real-time indicators may not be flashing red, the longer uncertainty reigns the more likely business investment slows, negatively impacting the labor market and ultimately spending. This tenuous period heightens the need for other policy offsets-namely stimulative fiscal policy – to partially mitigate the effects of tariffs and other policies.

Portfolio Strategy

Clients have recently asked us “What have you done?” or “What is your plan?”

First, our core belief is that globally diversified, multi-asset class portfolios enhance the investment opportunity set and are best suited for a variety of economic and market environments. Prudent diversification increases the likelihood of achieving long-term returns while also mitigating declines during short-term market disruptions.

Furthermore, over the last eighteen months we have made several changes and enhancements that are further aligned with these two objectives:

- Periodically reduced overweight equity allocations to rebalance to our clients’ asset allocation targets (adding to cash reserves or fixed income)

- Increased our allocation to quality companies (companies that exhibit high profitability, low debt levels, and earnings/cash flow consistency)

- Increased our allocation to Diversifying Assets (non-correlated investment strategies) for appropriate portfolios

- Replaced more concentrated, higher beta (risk) equity funds

- Increased credit quality in fixed income portfolios

These changes have also reduced underlying fund expenses and enhanced tax-efficiency.

Second, moving forward, we will increase our allocation to quality companies as defined above. We will also tax-loss harvest as opportunities present themselves. Tax-loss harvesting involves realizing a loss in one security and simultaneously swapping into a similar fund or ETF strategy to offset current or future capital gains. Moreover, we will continue to ensure appropriate levels of cash and liquidity for clients’ specific income and tax needs.

Additional portfolio changes we are considering:

- Shifting allocations within our global equity portfolio (within or across geographic, market cap, or style exposures)

- Increasing duration within fixed income portfolios if the yield curve continues to steepen

- Rebalancing incrementally to equity asset class targets

- Researching (and potentially adding) new non-correlating Diversifying Asset strategies

Uncertainty may reign in the near term. It’s still too soon to determine the outcomes and implications of global trade and fiscal policy and their long-term implications for equities, currencies and bond markets. Investors will need to navigate a variety of economic growth outcomes. This should keep volatility high, at least for a while.

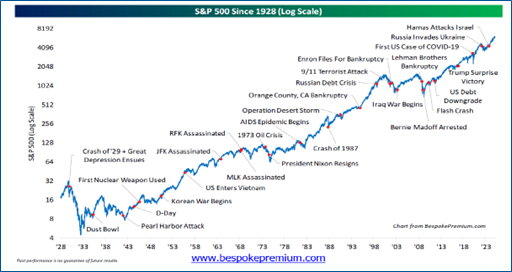

We advise you to remain disciplined and committed to your long-term investment plan and horizon. Furthermore, we strongly believe diversification will be as important as ever. Lastly, we remind you the U.S. stock market has endured wars, recessions, assassinations, pandemics, and other crises and ultimately reached new highs.

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,