Mon, December 30, 2024

In our second quarter 2023 commentary, we highlighted the low expectations investors had for market returns at the beginning of that year. Surveys of fund managers and investors were downbeat. Many economists were expecting a recession. For the first time in history, Wall Street strategists expected the S&P 500 to decline during the year.

As we head into 2025, we observe a vastly different picture. As of December 9th, the average Wall Street strategist target for the S&P 500 was nearly 10% higher with not a single strategist calling for a negative year.

Source: Strategas

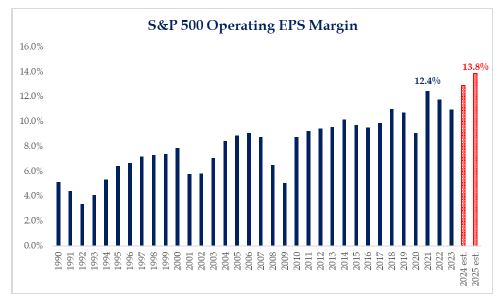

Earnings growth expectations are also robust. Analysts expect annual earnings growth to accelerate to 15% next year. This growth rate implies operating margins of 13.8%, an all-time high that would exceed the previous record by 1.4%.

Source: Strategas

Additionally, inflows to equity exchange-traded funds reached a record $114bn in November. It’s apparent that optimism and animal spirits are alive and well. One of the biggest risks in 2025 may simply be living up to these high expectations.

However, the sea change in sentiment doesn’t necessarily foretell a tough year for equities. Investors may be exuberant, but they are not irrational. The underpinnings of the economy and earnings are healthy. Consumer spending has been strong, especially during the second half of 2024, with real consumption growing at a brisk annualized pace of 3.7% in Q3 and an estimated 2.5-3.0% in Q4. Spending has been buoyed by growth in real after-tax incomes. While earnings growth expectations may be high, the absolute level of growth is still quite strong. Absent any further multiple expansion (a likely scenario), the market could move higher with positive earnings growth. Moreover, the U.S. economy may be in the early innings of a productivity boom spurred by automation and AI, supply chain innovations and changing workforce models.

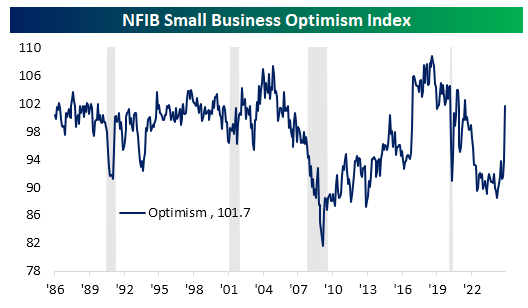

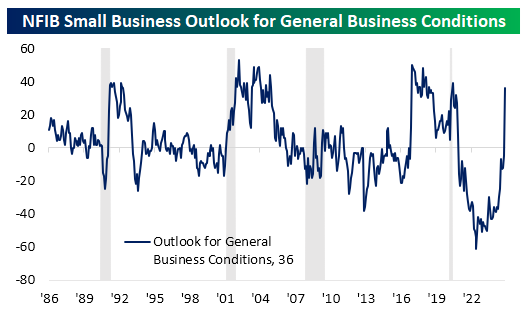

Additionally, renewed optimism is a welcome development for parts of the economy that have faced persistent challenges. For example, small businesses have been struggling with inflation, the high cost of capital, and a weak manufacturing economy. The November National Federation of Independent Businesses (NFIB) Optimism Index surged by the most since 1980. The percentage of firms planning to increase capex, and the NFIB hiring intentions index also jumped. Arguably, we should take this data with a grain of salt as much of the optimism resulted from the election and the potential for pro-growth policies such as lower taxes and de-regulation. Still, the enactment of such policies could unleash pent up demand from a vital part of the economy. Small businesses account for the bulk of hiring in the U.S.

Source: Bespoke Premium

Source: Bespoke Premium

Bottom line-expect more volatility in 2025. Higher expectations may mean stocks are more vulnerable to disappointments and less resilient to external shocks. Last week could be a harbinger of things to come. The Federal Reserve disappointed investors by reducing their forecasts for interest rate cuts next year. The Dow Jones Industrial Average fell 1,100 points (or 2.5%) only to rebound by several hundred points later in the week after the release of better-than-expected data on growth and inflation. 2025 could be another positive year for equities but one that will likely require more patience and fortitude than the last two years.