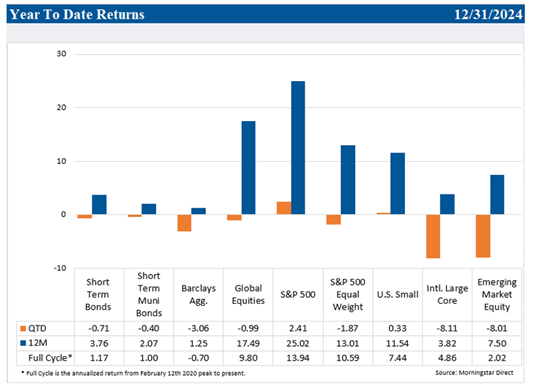

While stocks may have skipped a Santa Claus rally, they still delivered good returns for the year. For the first time this millennium, the S&P 500 rose more than 20% in two consecutive years. The U.S. economy continued to hum, and earnings growth accelerated. Despite ongoing wars, an eventful presidential election, and increased political uncertainty abroad, stock market volatility was the lowest in five years. What lies ahead? We’ll discuss our economic and market outlook after we review asset class performance. When all was said and done, 2024 didn’t look materially different from 2023.

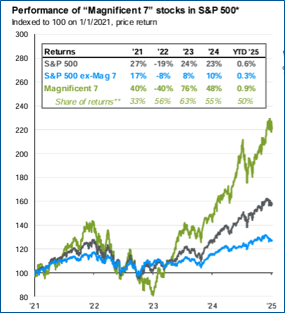

Markets in 2024 bore a close resemblance to 2023. A small group of mega-cap technology companies (The Magnificent 7, or Mag 7) again delivered the goods. The Mag 7 rose 48% as a group and accounted for 55% of the S&P 500 return. The remaining 493 companies rose 10% which was still a good absolute return. Additionally, despite better performance from small companies during the second half of the year, the gap between large and small companies was again wide, surpassing that of 2023.

The persistence of these trends can be explained primarily by differences in earnings growth. Mag 7 2024 earnings growth is estimated to be 34% compared to 3% for the remaining 493 companies. A similar earnings growth gap is expected between large and small companies. Additionally, investors bid up AI-related companies, expanding multiples in hopes of a continued ramp up in capital expenditures that may benefit select companies focused on AI-related infrastructure or implementation.

However, in 2025 the earnings growth gap between both the Mag 7 and S&P 493 and between large and small companies is expected to narrow considerably. We will revisit this topic later in the newsletter.

After performing well during the third quarter, both developed international and emerging markets suffered to close out the year. In the weeks leading up to and subsequent to the U.S. election, international equities came under pressure due to concerns around future trade policy, political uncertainty e.g. (Canada, Germany, and France) and renewed worries about Chinese economic growth. Additionally, the U.S. dollar rallied to finish the year at a multi-year high. Strength in the U.S. dollar was underpinned by uncertainty over trade policy, stronger U.S. economic growth, and widening interest rate differentials between the U.S. and international markets.

Bonds had a volatile year. As seen in the chart below, the path of the 10-year yield resembled a roller coaster ride. Shifts in the inflation and employment outlooks and the Fed’s messaging caused volatility throughout the year. Yields spiked during the first part of the year as disinflation stalled, and the Fed affirmed its “higher for longer” stance. Weakness in the job market and renewed progress on inflation (including a negative month-over-month CPI number in July) led to a precipitous decline in yields over the summer. The Fed signaled and then delivered on policy easing with a larger than expected first interest rate cut of 0.5% in September. The 10-year yield finished 2024 near the highs of the year due to resilient economic growth, renewed stickiness in inflation, and concerns about potential fiscal policy under the new administration.

Diversifying assets provided steady returns that exhibited little to no correlation with equities or bonds. The group posted returns between those of bonds and stocks, in line with our long-term expectations. The reinsurance fund had another strong year. Like 2023, the fund benefitted from robust premium income and a relatively benign level of insured claims. We were also pleased with the initial performance of the multi-strategy fund we purchased earlier in the year.

Looking forward, the underpinnings of strong economic growth and rising corporate profits are reasons to be optimistic, but there are potential headwinds that may keep markets in check.

The U.S. Economy: On Solid Ground to Start the Year

The U.S. economy once again exceeded expectations in 2024 led by a surprisingly resilient labor market and strong consumer spending. After a slow start to the year, consumption picked up briskly. During the second half of the year, real consumption grew nearly 3.5% with particularly strong spending on services such as travel and dining. Consumption was supported by continued growth in real wages. Business investment in technology, automation, and infrastructure and ongoing investments from the Chips Act and Inflation Reduction Act also contributed to growth.

Economic growth was consistent with quarter-over-quarter real GDP growth of 1.6%, 3.0%, 3.1%, and an estimated 3.0% during the most recent quarter. While growth may moderate in early 2025, we are entering the year on a solid footing as evidenced by the December employment report which significantly exceeded expectations.

Earnings Growth: Strong and Broadening

The macro backdrop supported accelerating earnings growth in 2024. According to data provider Factset, S&P 500 earnings are expected to have grown 9.4% in 2024, up from 1.4% in 2023.

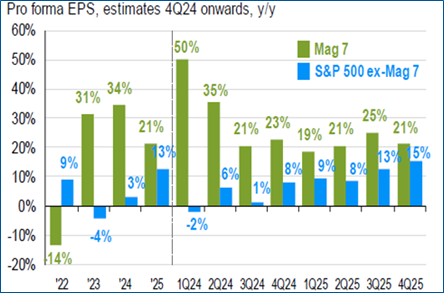

While expectations of nearly 13% profit growth in 2025 are admittedly a high bar to clear, the absolute level of growth is still strong and even absent any further multiple expansion (a likely scenario) could support higher prices.

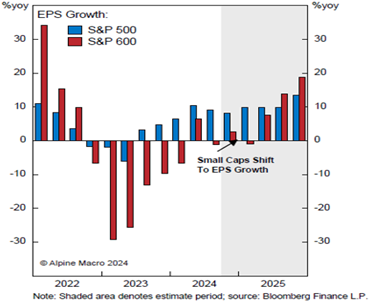

Moreover, earnings growth is set to broaden. The Mag 7 vs. ex-Mag 7 earnings growth gap is expected to narrow from 31% in 2024 to 8% in 2025. Small company earnings are also expected to accelerate and may shift to several quarters of positive growth. This development may explain the more competitive performance of small companies during the second half of the year.

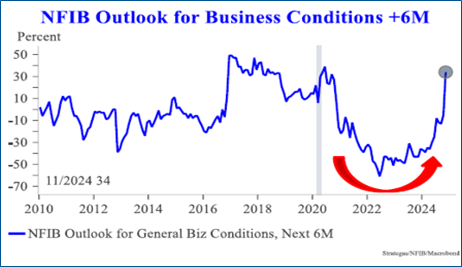

Small Business Optimism: Mr. Mojo Rising

Many recent surveys show a surge in confidence and optimism across corporate America, especially among small businesses. This is a promising development since small businesses have been disproportionately affected by higher interest rates and inflation. Moreover, small businesses are responsible for most of the hiring in the US. Admittedly, this renewed optimism has occurred since the election and reflects hopes for future pro-growth policies such as tax cuts and deregulation. Nonetheless, these “animal spirits” represent a potential catalyst for growth from an important sector of the economy.

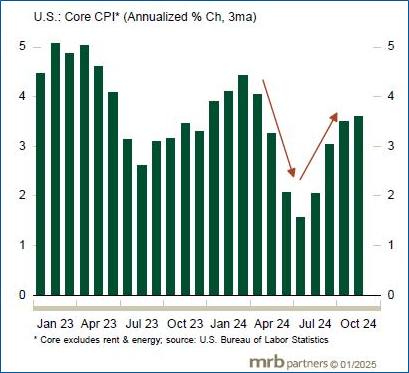

The Inflation Genie May Not Be in the Bottle

The biggest risk for markets this year may be sticky inflation. Inflation fell throughout 2023 and for most of 2024. Goods inflation fell precipitously due to the unwinding of post-pandemic distortions in supply chains. A surge in immigration may have helped moderate wage growth. These two tailwinds will likely abate this year. Moreover, the objective of the Federal Reserve’s aggressive monetary policy was to reduce aggregate demand to lower inflation further. Instead, economic growth has been and may continue to be resilient, especially if the Trump administration moves forward with pro-growth, stimulative fiscal policies.

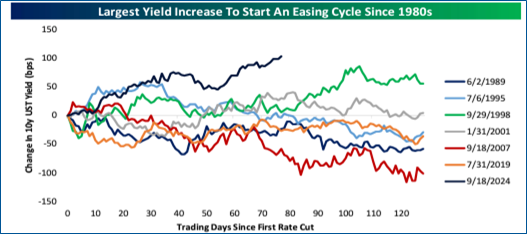

Bond Yields: A Retest of 5%?

With inflation still uncomfortably higher than the Federal Reserve’s (Fed) 2% target, the Fed has reined in its rate cut expectations for 2025. The Fed now projects two cuts, down from four earlier in the year with a possibility they will rein in expectations further. Bond yields have retraced most of their summer decline.

The 10-year treasury yield rose nearly 1.2% from the low of 3.62% in mid-September. In fact, this represents the largest increase in the 10-year yield from the onset of an easing cycle since the early 1980s.

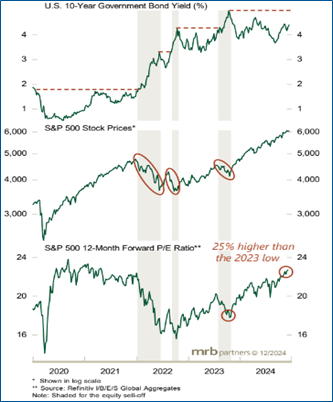

Past spikes in yields have typically led to volatility in equities. Thus far, stocks have mostly taken the rise in yields in stride. However, a retest of a 5% yield on the 10-year Treasury would likely cause some turbulence. Fiscal policy will also have an influence. The bond market may react negatively to policies it believes will overheat the economy. Equities will likely continue to take their cues from bond yields over the coming weeks and months.

Balancing the various tailwinds and risks, our view is the weight of the evidence suggests stocks are still on a solid footing. Ultimately, strong economic and earnings growth matter and should underpin markets.

We are likely to witness headline-induced volatility over the coming weeks and months. We categorize the Trump administration’s policies as “known unknowns.” We know that changes are coming for trade and fiscal policy, immigration, and regulation. We don’t know exactly what form they will take nor their precise timing. Moreover, we can make the case for certain policies tilting growth to the upside and others to the downside. We may see a mix of both. For example, tariffs may be offset by tax cuts for small businesses. Despite the headlines, we maintain our view that the new administration does not want to destabilize markets or the economy nor do they wish to reignite inflation.

We also believe U.S. equities will continue to lead global markets. The performance gap between the U.S. and the rest of the world can also be explained by differences in profitability and earnings growth. This gap may persist. Europe for example may continue to face structural challenges such as lack of innovation, lower investment in R&D, regulation, and fiscal austerity. With the Fed taking a wait and see approach while the European Central Bank continues to ease, the U.S. dollar may remain strong. Additionally, we maintain our cautious view on China. While the Chinese government appears to be more willing to address the country’s numerous structural challenges, their ability to sustainably improve economic growth with sufficient fiscal stimulus remains to be seen.

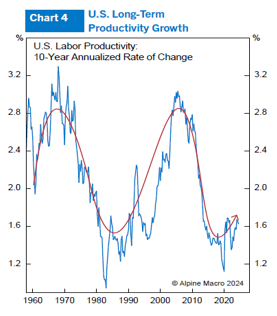

Conversely the U.S. may be in the early innings of another productivity boom catalyzed by AI, automation, workforce efficiencies, supply chain improvements, and a surge in small business creation since the pandemic.

In summary, we believe our portfolio strategy of balance and diversification should provide resilience in a variety of economic and market environments. We are also diligent in ensuring that your portfolios are aligned with their long-term objectives and provide sufficient cash flow and liquidity based on your unique needs.

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,