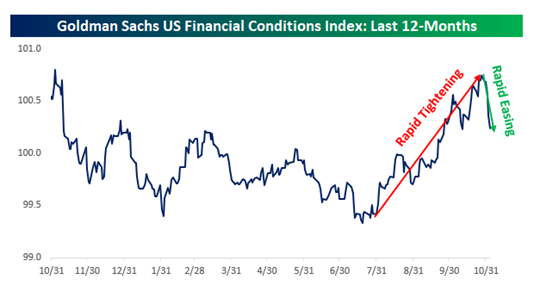

Markets played their own version of the popular children’s game “Red Light, Green Light” during the fourth quarter. After the Fed’s “higher for longer” forecast in September, both stock and bond markets swooned. The S & P 500 briefly entered correction territory in October while the more interest rate sensitive Russell 2000, an index of small companies, corrected nearly 18% from its mid-summer high. Bond yields spiked with the 10-year Treasury bond yield eclipsing 5% in mid-October. These events caused a rapid tightening in financial conditions, a development that has historically preceded an eventual downturn in the economy. Investors feared that to combat above-target inflation, the Fed would keep rates in restrictive territory for too long and resist responding to future economic weakness with policy easing. This was the “red light.”

However, the Fed’s messaging changed quickly as the quarter progressed. In the November FOMC statement, the Committee acknowledged the tightening of financial and credit conditions would likely weigh on economic activity. During their public appearances, several Committee members suggested the Fed was at least done hiking. In late November, Federal Reserve Governor Christopher Waller stated “I am increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2 percent.”

Then, remarkably in the December FOMC statement, the Fed pivoted to forecasting an outright easing cycle in 2024. The Committee implied three interest rate cuts in 2024, up from two in the September forecast (which incidentally had been reduced from four at that meeting). The primary reason for this pivot? Continued progress on disinflation, a development we discussed in our last two quarterly commentaries. In a mirror image of 2022, inflation appears to have surprised to the downside in 2023. In the December statement, the Fed lowered its fourth quarter core PCE (Personal Consumption Expenditures) forecast to 3.2% from September’s 3.7% projection. We expect continued progress on this front going forward. In fact, over 50% of underlying core PCE components are already at the Fed’s target of 2%. Financial conditions eased almost as quickly as they had tightened. This was the “green light.”

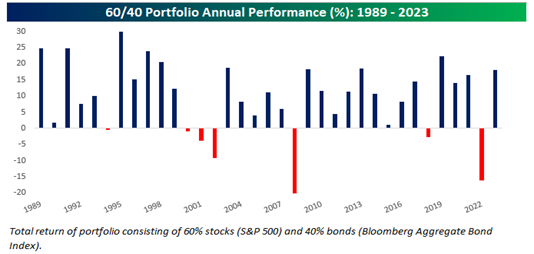

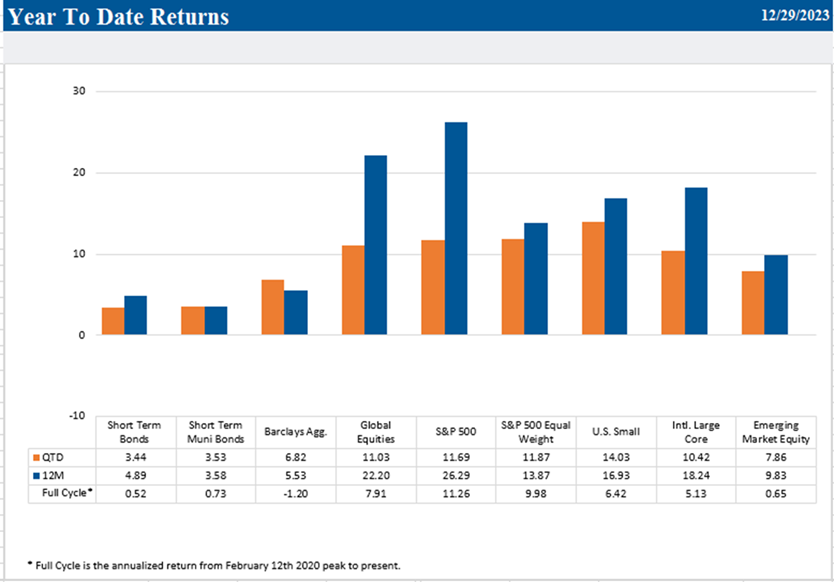

Equity and bond markets cheered these developments. The combination of disinflation, moderate economic growth, and a more accommodative Fed has typically been an optimal environment for both equities and bonds. The S & P 500 returned just over 11% for the quarter, rallying 16% from its October 27th low. The Russell 2000 delivered a 14% return, snapping back nearly 24% from its low point. Developed international stocks also performed well, particularly in Europe, while emerging markets posted more modest returns as they continued to be weighed down by China. While the performance of most global equity markets was impressive, the performance of bonds was historic. The Bloomberg Barclays Aggregate, a broad index of investment grade fixed income, had its best two-month performance ever to close out the year.

If one were to assign a movie title to asset class performance in 2023, it might be “The 60/40 Portfolio Strikes Back.” As we discussed in our mid-year review, the mood was downright gloomy to start the year with many investors expecting a recession and persistent inflation. Average Wall Street projections for S & P 500 returns were negative for the first time ever. The double-digit return of a 60/40 portfolio likely surprised many.

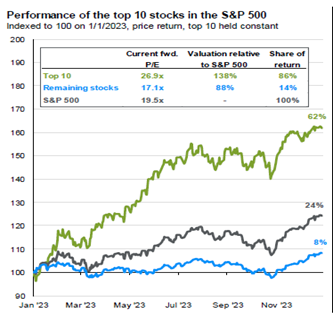

However, looking under the hood, the big story of 2023 was the contribution of several mega-cap technology companies (often referred to as the “Magnificent 7”) to the U.S. market’s return.

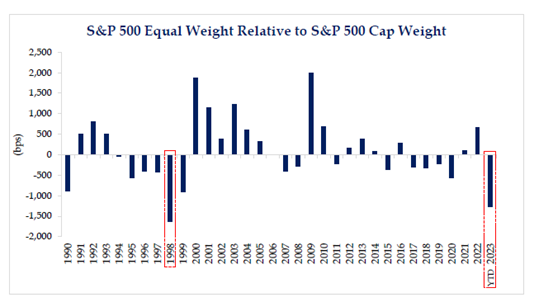

The market cap-weighted S&P 500 nearly doubled the return of its equal-weighted counterpart. Additionally, the weighting of the top 10 stocks ended the year close to a record high, easily surpassing the same measure from the late 1990s. However, market breadth improved during the fourth quarter, as seen in the performance of small companies and beleaguered sectors such as financials. We remind readers of the parallels to the late 1990s. After that period of mega-cap dominance, the equal-weighted index outperformed the market-cap weighted index for several consecutive calendar years. History may not repeat itself, but it often rhymes.

Developed international stocks posted strong absolute returns but did not keep pace with US stocks. Emerging markets stocks also rose with strength in Latin America and India offset by a difficult year for Chinese shares. Recall earlier in the year we liquidated your China-focused fund, reduced our allocation to emerging markets and reallocated that capital to high quality, large-cap domestic stocks.

While more interest-rate sensitive fixed income strategies did not reward investors for the first ten months of the year, November and December more than made up for this. The Bloomberg Barclays Aggregate returned 5.53% for the year with a nearly 7% return in the fourth quarter. Short-term investment grade taxable bonds returned just under 5% for the year. Credit sensitive fixed income, whether it be investment-grade corporate bonds, high yield bonds, or mortgage-backed securities, also delivered strong returns. Thus, despite the relatively persistent volatility seen in fixed income markets, it ended up being a really good year. Remarkably, despite the tumult, the 10-year Treasury yield ended the year almost exactly where it started!

Most diversifying strategies performed well, particularly reinsurance which was aided by a robust premium pricing environment and a benign level of insured loss claims. The alternative income strategy benefitted from higher levels of earned income. After a strong 2022, private real estate declined due to higher interest rates and lags in appraisal values, but our fund maintained a stable income yield.

Moderate growth, disinflation, and less restrictive monetary policy should continue to provide a positive backdrop for equities and bonds. Growth continues to be buoyed by consumption and fiscal stimulus while forward-looking indicators imply continued progress on the inflation front. Additionally, the Fed appears more likely to ease policy if inflation continues to fall or the labor market weakens.

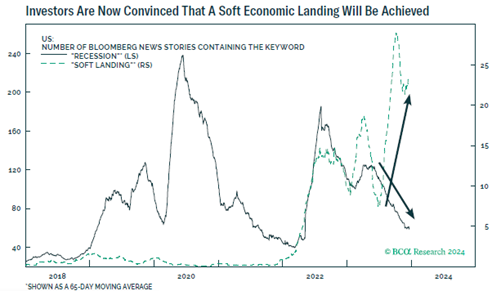

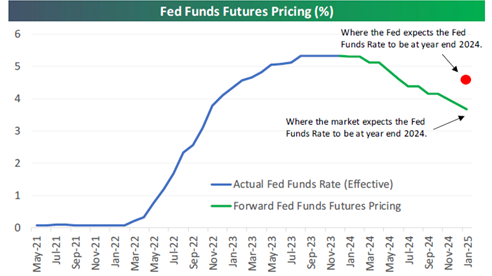

However, while the Fed’s pivot may have reduced the odds of recession, the steep rally in equities likely priced in some of this narrative, also reducing the margin for error. As more investors subscribe to the soft landing scenario, equity markets may be faced with expectations that are too optimistic just as they were too pessimistic just twelve months ago. Similarly, the bond market expects over six interest rate cuts in 2024, far from the Fed’s implied three. This gap widened after the pivot in mid-December. Any stall in the disinflation process and/or willingness by the Fed to push back against easier financial conditions could cause a repricing in expectations, introducing renewed volatility in fixed income markets. Additionally, the economy, while quite resilient in 2023, exited 2024 with signs of slowing. Despite the Fed’s pivot, rates will still be restrictive for a period of time, adding more pressure to the lagged effects of prior policy.

We believe market breadth will continue to expand as investors begin to favor less expensive areas of the market. While the top 10 stocks in the S & P 500 trade at 26.9x forward earnings, the remaining 490 trade at a more reasonable 17.1x. The broadening of the market may benefit developed international indices which are far less top-heavy than those in the US. While yields may retrace some of their recent declines, we are still optimistic on fixed income due to continued disinflation, a cooling economy and still attractive yields. Bonds should resume their role of providing portfolio ballast during times of equity market volatility.

The conflict in the Middle East may escalate. Further escalation could disrupt global shipping and stress supply chains. Approximately 12% of global trade and 30% of container shipping flows through the Suez Canal. The extent and nature of Iran’s involvement will continue to impact oil prices. Furthermore, the ongoing war in Ukraine, potential China/Taiwan tensions, and our own highly unpredictable Presidential election cycle each has the potential to cause market volatility. While they are unsettling, geopolitical events are difficult to handicap and should not dictate material changes to a strategic, long-term asset allocation.

This month we will implement several changes to your international equity portfolio. We believe this realignment will achieve several objectives. First, it should provide an effective balance across geographies, markets capitalizations, and styles. Second, the realignment prioritizes higher conviction managers, both within developed and emerging markets, whom we believe have demonstrated consistent relative performance in both up and down markets. Third, it realizes our overarching objective of reducing expenses and increasing tax-efficiency.

However, overall we continue to tilt towards US companies within your global equity portfolio with a specific bias towards companies that exhibit high profitability, low leverage, and earnings quality and consistency. Within fixed income, we maintain a high quality, investment-grade bias with a tilt towards intermediate-term bonds. Diversifying strategies should continue to provide valuable benefits to portfolios. We expect diversifying strategies to deliver long-term returns between fixed income and global equities, exhibit low correlations to each asset class, and thereby reduce overall portfolio volatility.

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,