Tue, October 15, 2024

The path to higher asset prices during the third quarter was eventful and at times dramatic. An historic spike in volatility in early August led to a swift decline in stocks that ended almost as quickly as it began. Fears of an economic hard landing earlier in the quarter receded as data on consumer spending and employment suggested a downturn was not imminent. The Federal Reserve began to lower interest rates, while Chinese authorities turned on the stimulus spigot. Tensions rose in the Middle East, while the U.S. Presidential election was rife with twists and turns few could have predicted at the beginning of the quarter. Nonetheless, global equities moved higher with several markets closing out the quarter at or close to all-time highs. Bonds and diversifying assets also delivered good returns. It was a fruitful quarter for most asset classes.

Asset Class Performance Review

U.S. Equities

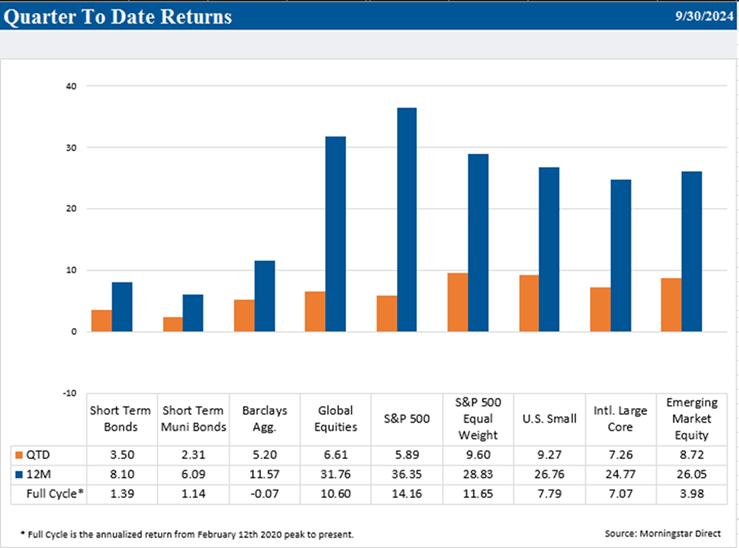

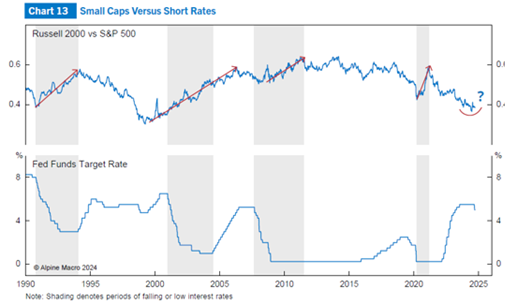

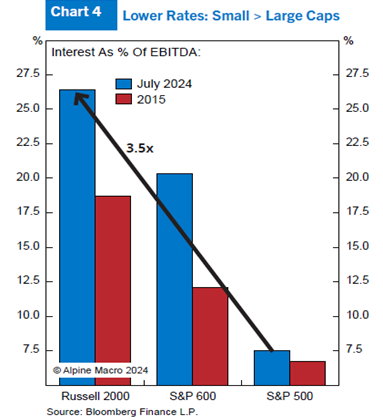

Investors began to rotate towards small and mid-sized companies and value stocks. In last quarter’s commentary, we discussed how smaller companies should benefit from lower rates given their greater dependence on debt to fund growth and higher use of floating-rate debt (where interest payments reset with short-term interest rates).

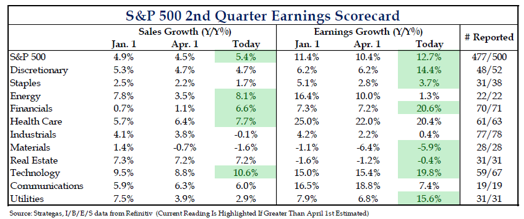

Furthermore, while better than expected earnings growth was a tailwind for the overall U.S. market, the broadening of profit growth increased investor interest in value stocks. Second quarter year-over-year earnings growth for S&P 500 companies grew 12.7% versus the April 1st estimate of 10.4%. The technology and communication services sectors contributed the lion’s share of overall earnings growth over the last several quarters. During the recent quarter, we saw more significant contributions from financial stocks, healthcare, and utilities.

International Equities

For the first time in nearly two years, both developed international and emerging markets stocks performed better than U.S. stocks.

The U.S. Dollar Index declined nearly 5% during the quarter as yields dropped and investors considered the prospects of additional monetary policy easing by the Fed. Developed international funds typically hold higher weightings in value stocks and likely benefitted from rotation into these sectors. Another key catalyst emerged late in the quarter in what many are referring to as China’s “whatever it takes” moment. This year marks an important milestone for the country-the 75h anniversary of the founding of the People’s Republic of China.

In a surprising move, given their previous reticence for large-scale stimulus, the Chinese central bank and federal regulators announced significant stimulus programs targeting the banking sector, the property market, and the stock market. These reactionary measures were taken to stem accelerating economic weakness and ailing markets. The actions in the banking sector were more incremental and included cutting rates, lowering reserve requirements to boost lending, and injecting capital into state banks. The measures targeting the property and equity markets initially appear to be more substantial. The central bank set up a swap facility that will provide direct financing to securities dealers, funds, and insurance companies to purchase stocks.

Additionally, the central bank set up a facility that will allow state-owned firms buying unsold property to finance up to 100% of purchase amounts directly from the central bank.

While it’s encouraging to see the Chinese government begin to address their many challenges in a more meaningful way, they likely had no choice. The economy was falling further into a deflationary spiral. The measures taken may succeed in stabilizing the economy in the near-term, but we are initially skeptical they will sustainably improve growth or remedy longer-term structural issues.

Fixed Income

Bonds delivered positive total returns during the quarter as lower inflation and the prospects for monetary easing led interest rates to decline across the yield curve. The 2-year and 10-year treasury yields fell over 100 basis points and 60 basis points respectively. Funds with longer durations (more sensitivity to changes in interest rates) performed best. Credit conditions remained benign with spreads hovering near cycle lows. We continue to be optimistic on the prospects for bonds but would not be surprised to see rates increase in the near term as investors reassess the resilience in the U.S. economy and the implications for monetary policy.

Diversifying Assets

Diversifying assets also performed well. Each fund in the TFC strategy was positive with reinsurance delivering the best return. Thus far, the U.S. hurricane season has not been a significant event for the reinsurance industry. Estimated Insured claims from Hurricane Milton are more modest than original projections.

Outlook and Portfolio Strategy

Fear the cut… or not?

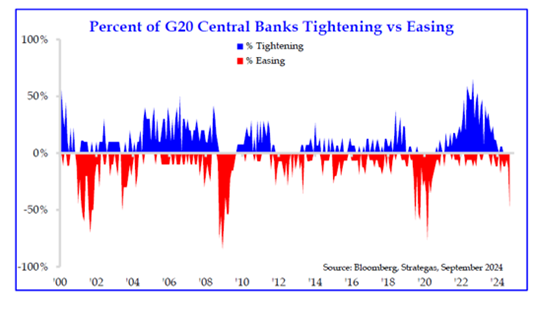

The soft June and July employment reports and the significant downward revision (-818,000) to payroll growth in the 12 months ending in March spurred the Federal Reserve to begin its easing cycle with a larger 50 basis point cut. The Fed also updated its economic and interest rate projections, implying an additional 50 basis points of easing in 2024 and 100 basis points in 2025. Falling inflation also gave the Fed cover. The core PCE deflator (the Fed’s preferred gauge) rose just 0.13% in August, the fourth straight month the measure has come in at an annualized rate below 2%. With the Fed now easing, most developed country central banks are lowering rates-the reverse of just two years ago.

Stocks have historically performed well in the period between the last rate hike and the first rate cut. The recent pause was the second longest in terms of duration but the strongest pause in terms of return. However, equity performance has been more mixed during easing cycles. Should we fear the cut?

The simple answer is it depends on whether future interest rate cuts are associated with a recession. Easing cycles during non-recessionary periods (e.g. 1995, 1998) led to strong market returns while easing cycles during recessions (2001, 2007) did not.

To assess the current cycle, we focus on the U.S. consumer. Consumer spending accounts for 70% of the U.S. economy. Both economic and market-based indicators suggest the current state of and outlook for consumer spending is positive.

After a sluggish start to the year, spending picked up over the summer. The annualized rate of growth in the three months to August for the control measure of retail sales (a measure which strips out more volatile components) rose 5.7%, from 4.9% in July. Real (inflation-adjusted) consumer spending may have grown 3% in Q3. The future expectations index within the September Michigan consumer sentiment survey implies consumption should remain robust.

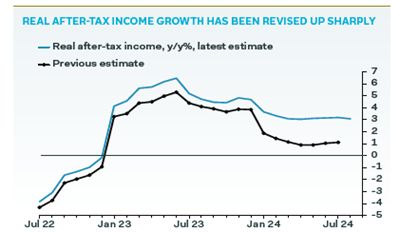

Furthermore, we received news during the quarter that the consumer may be in better shape than previously thought. The Bureau of Economic Analysis revised up personal income for Q2. The revision boosted the savings rate from 3.3% to 5.2%, suggesting consumers have more dry powder than originally estimated.

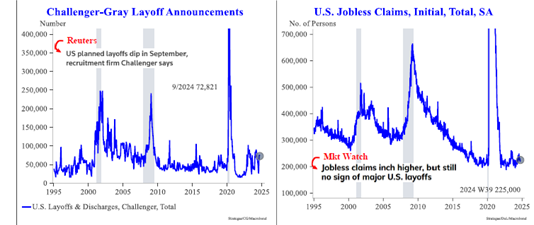

Robust consumer spending may continue to offset weakness in other parts of the economy such as manufacturing and housing. The key going forward is the health of the labor market. Leading indicators such as the National Federation of Independent Businesses survey and JOLTS (job openings) point to a continued downshift. For now, wages are holding up, and while hiring has cooled, layoffs have remained low. Another risk is oil prices. A dollar more spent at the gas pump is a dollar less spent somewhere else. Low gas prices have been a tailwind for the consumer over the last several months. However, potential disruptions in oil supply in the Middle East could change that.

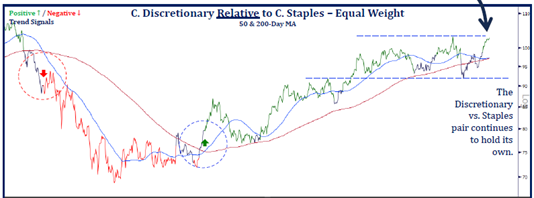

One of our research providers describes the chart below as one of its favorite economists. The chart shows the performance of an equal-weighted index of consumer discretionary stocks relative to a similar index of consumer staples stocks. Consumer discretionary stocks (e.g. travel, dining, luxury, home furnishings) are far more sensitive to changes in employment and the economy than consumer staples (household products, basic food necessities). Historically, the relative performance of the two groups has been a good barometer for investors’ outlook on consumer spending and the economy more broadly. The ratio has been in a rising trend since the market bottom in 2022.

Portfolio Strategy

We are encouraged by the recent broadening of the market into small and mid-sized companies and value stocks. This rotation should benefit our approach to equity investing, which emphasizes diversification across sectors, styles, and market capitalizations. Despite the apparent will to stimulate the Chinese economy, we will continue to underweight China and emerging markets more broadly until we see sufficient signs that policy will begin to remedy longer-term structural challenges.

During the quarter, we rebalanced fixed income portfolios to enhance diversification, increase after-tax yields, and reduce expenses while maintaining our emphasis on high quality bonds.

We continue to believe diversifying assets will provide valuable portfolio benefits and recently changed your investment reports to provide more insights into portfolio allocations and performance.

Thoughts on the Election

With less than three weeks to go before the election, many clients are asking our opinion on how the outcome will affect markets.

We offer three thoughts:

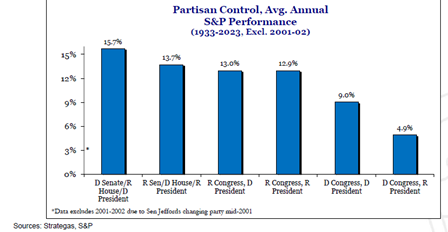

First, in the long run, stocks have increased regardless of who is in control. The economy has continued to grow, and corporations have successfully grown profits in a variety of political, regulatory, and tax regimes. This may sound simplistic, but history has borne this out.

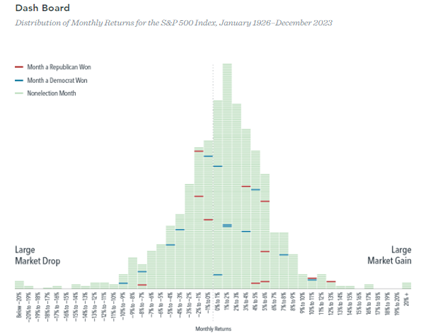

Second, elections can cause short-term volatility, but stock returns in election months have not been that different from returns in any other month. Furthermore, the distribution of positive and negative returns in election months has been roughly even.

Third, enacted policy is usually much narrower than what is announced on the campaign trail. Harris and Trump do differ substantively on key economic issues such as trade, taxes, regulation, and the budget. The likelihood of each candidate’s more controversial platform policies ultimately getting passed is low, especially if there is a divided Congress. Admittedly, a sweep of either party could change that dynamic.

We aren’t discounting the election’s importance in a variety of areas but wish to provide market perspectives as we near the finish line. Moreover, we hope these insights are a helpful reminder to remain committed to your long-term investment plan regardless of the outcome. Please join us for a webinar on November 14th for a discussion on the implications of the election for markets and the economy. We will be sending out invitations shortly.

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,