Thu, March 6, 2025

As avid college basketball fans, each year we look forward to March. The NCAA basketball tournaments never fail to deliver-the excitement of the early round games, the drama of the Final Four, the Cinderella stories, the buzzer beaters, our usually busted brackets. However, as investors and asset allocators, March hasn’t always been as enjoyable. Throughout our careers, we have witnessed the rescue of Bear Stearns, the Fukushima earthquake, Covid, the failure of Silicon Valley Bank and the regional bank crisis-each uniquely distinct events that occurred in March. What is it about this month? There’s something to that “In like a lion…” quote.

This March has provided another bout of market volatility. Tariffs have progressed from headlines and threats to actual implementation. Despite President Trump’s stated intentions to downsize government, investors have been surprised by the speed and scope of the actions taken by DOGE and other government agencies. The seemingly constant flow of headlines, threats, and reversals has unnerved investors.

The coming weeks and months may continue to be difficult as the U.S. economy experiences what is often referred to as a “growth scare.” A growth scare is a sudden fear that economic growth will weaken or decline. Over the last decade, the U.S. has experienced a growth scare about every 2-3 years, with each brought on by different catalysts. In 2015-2016, markets swooned (two 10%+ corrections within a few months) when investors feared a collapse in Chinese economic growth would cause a global recession. During Trump’s first term, U.S. stocks fell nearly 20% in a matter of weeks in late 2018. During this period, the Federal Reserve was raising interest rates while the economy slowed, primarily due to trade tensions with China. Three years ago, high inflation caused the Federal Reserve to embark on its most aggressive interest rate hiking cycle since the 1980s. Stocks fell 25% from January through October that year. However, as difficult as it may have been to weather each period, the U.S. avoided recession, stocks stabilized, and subsequent returns were quite strong. While it is premature to make a recession call, the risks of one are rising.

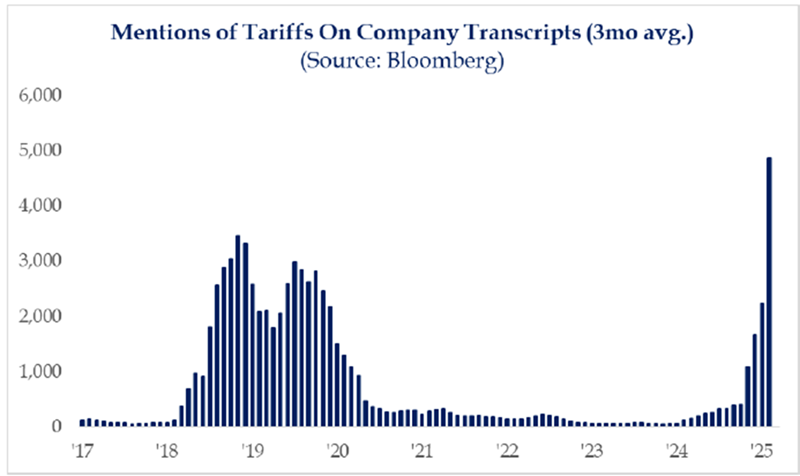

We believe the impetus for the current growth scare is a sudden and sharp decline in consumer and business confidence. Readings from two widely followed consumer sentiment and confidence surveys have shown a swift drop in both consumers’ assessment of current conditions and of future expectations. The latter correlates highly with subsequent consumer spending. Mention of tariffs on company earnings calls has surged. This uncertainty may cause companies to reduce capital expenditures and/or hiring. Thus, investors are questioning the durability of two significant underpinnings of this bull market-consumer spending and corporate earnings growth. Note that for the most part the consumer-related data has been “soft” (subjective) as opposed to “hard” (objective) data. Additionally, while corporate earnings estimates have yet to be revised down materially, we expect more conservative guidance from companies in the coming weeks. We will continue to diligently monitor these and other data points.

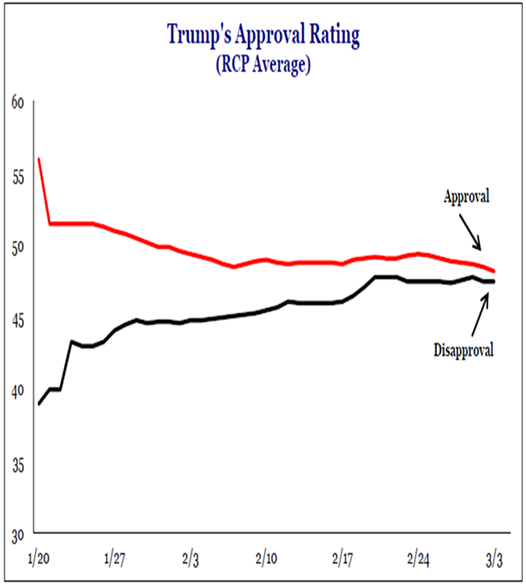

Moreover, while we acknowledge the inherent unpredictability of President Trump’s approach and strategy, we offer two observations which may provide some perspective. First, unlike Trump’s first term, the trajectory of policy currently is “mostly spinach now, candy later.” (paraphrasing a quote from one of our research providers). His first term started with a flurry of pro-growth, pro-market policies such as the Tax Cuts and Jobs Acts of 2017. The tariffs came later in 2018-2019. This time around, markets are grappling with trade policy first. However, we are reminded that later this year we may see an extension of tax cuts, potential new tax cuts, and ongoing tailwinds from deregulation and lower energy prices. Second, while Trump appears to be less influenced by markets (and his approval rating) during his second term, we believe he ultimately pays attention. Perhaps it’s no coincidence that he initially delayed tariffs on Mexico and Canada during the brief market swoon in early February and today exempted many goods (until April 2) covered by the tariffs that took effect early this week. The S&P 500 index has lost its post-election gain while Trump’s approval rating has declined. Nonetheless, the administration appears willing to take on more economic risk than investors previously thought.

We conclude with an important reminder that portfolio diversification has and should continue to pay off. Our investment strategy of building well-balanced portfolios that are diversified across and within asset classes may be particularly beneficial in the current market environment. For example, while U.S. equities are essentially unchanged year-to-date, several international currencies and markets have risen sharply. Within U.S. equities, market breadth has rotated from mega-cap technology stocks to large-cap quality and value stocks. Despite tariff fears, bonds have rallied as interest rates have declined. Unlike 2022, bonds should provide more yield and ballast as the economy slows. We expect diversifying assets (in most client portfolios) to remain stable given their low correlation to equities. Reflecting once again on the NCAA basketball tournaments, past champions have rarely featured just one star player-rather a healthy mix of offense and defense.

Successful investing is a long-term game of patience and discipline. We will keep you informed with additional communications and another investment webinar in April when there may be more clarity on tariffs, other policy initiatives and their potential economic and market implications.

Sincerely,

Renée Kwok, CFP®

President, CEO & Shareholder