Mon, July 15, 2024

Disinflation Strikes Back:

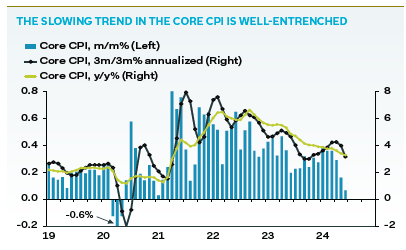

The April, May, and June Consumer Price Index (CPI) data likely put to rest fears of a dreaded second wave of inflation. Conversely, the disinflation process may have resumed in earnest. The June headline CPI actually declined -0.1% month-over-month while the core CPI rose a modest 0.1%. The June data showed widespread disinflation. Rents, which have been the stickiest component, rose by the smallest amount since April 2021. Core goods prices fell -0.1%, led by declines in both new and used vehicles. Furthermore, the June employment report showed that year-over-year growth in average hourly earnings grew at the slowest pace in three years. The recent inflation data open the door for the Fed to begin cutting interest rates in September. Good news, right? Maybe so, maybe not. Inflation is falling in part because the economy is weakening. We will return to this topic, revisit the economic landing scenarios we reviewed last quarter, and discuss the implications for portfolio strategy later in this commentary.

Second Quarter Performance Review

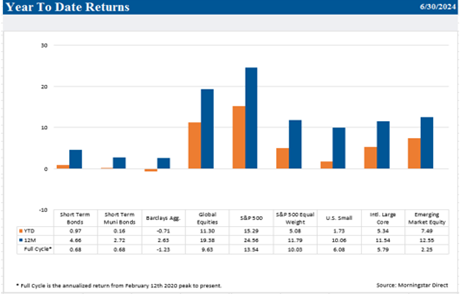

During the second quarter, better than expected corporate earnings growth and renewed progress on inflation led to generally positive, but widely divergent, global equity returns.

U.S. Equities

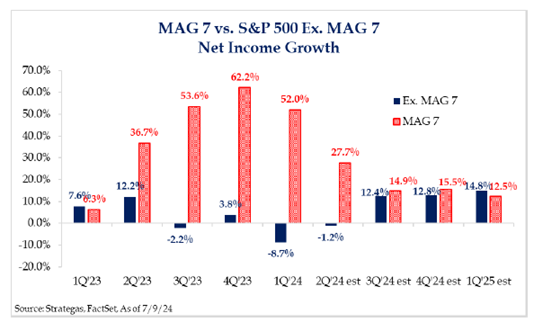

Market breadth narrowed considerably, especially in June. While the Russell 1000, an index of the 1000 largest U.S. companies, rose 3.4%, the average stock in the index fell 4.2% during the quarter. One stock, Nvidia, accounted for nearly 50% of the advance, and the Fab 4 (rebranded from the Magnificent 7) accounted for 120% of the return. The Russell 2000, an index of smaller companies, declined 3.3%. Large company value stocks trailed large company growth stocks by nearly 12% during the quarter. The U.S. market is as top heavy as it has ever been with the weighting of the top 10 stocks approaching 40%, far exceeding the same metric from the late 1990s.

A broadening earnings recovery may stall, or potentially reverse, this trend. Stock performance tends to correlate highly with the direction of earnings estimates. As the year progresses, the year-over-year earnings growth of the S&P 493 (i.e. the index outside of the Magnificent 7) is expected to catch up with the growth rate of those heavily weighted stocks. Additionally, the same dynamic is expected to occur with small company earnings relative to large companies. Lower interest rates and inflation could provide a significant tailwind for small companies. Small companies are more dependent on the debt markets to fund growth, often utilize floating rate debt (where interest payments reset with short-term interest rates) and have a greater percentage of debt maturing in 2025.

Note that during July, we have witnessed an historic rotation from large-cap technology stocks such as Nvidia into small-cap stocks. This rotation was kick-started by the June CPI report, likely reflecting the tailwind that lower inflation and interest rates may provide these companies.

International Equities

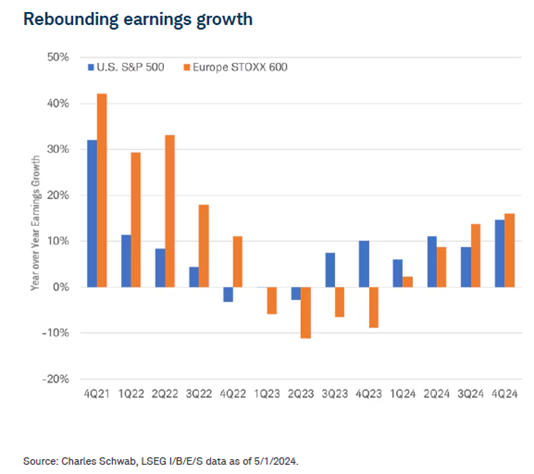

Developed international markets also exhibited widely divergent performance. European markets started the quarter strong, but their rally fizzled out in June, primarily due to political uncertainty caused by the elections in France. The European economy exited a mild recession early this year. While the manufacturing recovery has been uneven, the service economy has improved. Falling inflation has led to positive, real wages. Tourism has reached pre-pandemic levels.

In addition, while consumer excess savings in the U.S. are nearly depleted, European households have a significant amount of excess savings. These factors should bolster consumer confidence. Year-over-year European earnings growth relative to the U.S. may also experience some catch-up later this year.

The Japanese Nikkei 200 market advanced in local currency terms. However, the gains were erased in U.S. dollar terms as the Japanese yen reached an all-time low, causing the Bank of Japan to intervene. On a year-to-date basis, Japanese equities are still one of the best performing developed international markets even when adjusting for currency movements. Emerging markets were a bright spot during the quarter, with gains led by India and China. The Chinese government has continued to target weakness in the property and real estate sectors, but the underlying trends (falling home prices, sales, and starts) will continue to subdue domestic demand. China’s second quarter GDP growth was below expectations, and new home prices fell by the most in nine years.

Fixed Income and Diversifying Assets

Bonds rallied in June as a slew of weaker than expected economic data and better inflation data caused yields to decline across all maturities. For the quarter, most fixed income strategies delivered slightly positive total returns. Diversifying assets were mixed with continued strength in reinsurance offset by a decline in alternative income.

Second Half Economic and Market Outlook

BCA Research recently compared economic cycles to phase transitions that occur in the natural world. More specifically, if one were to place a warm glass of water in a freezer, its temperature will gradually decline until the water freezes, turning from a liquid to a solid. Nothing else needs to happen; the only requirement is for the freezer’s temperature to remain below 32 degrees Fahrenheit. To compare this phase transition to the current economic cycle, BCA likens the temperature in the freezer to tight monetary policy. The only condition necessary for the economy to eventually freeze is for monetary policy to remain tight (i.e. for interest rates to remain high) for a sufficient period of time. (Third Quarter 2024 Strategy Outlook: Here Comes the Pain, Peter Berezin, BCA Research).

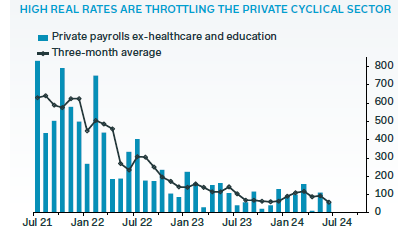

It’s evident that the economy, like the water in the freezer, is cooling as an extended period of tight monetary policy begins to weigh on growth. In last quarter’s commentary, we highlighted leading indicators, specifically among small businesses, that suggested a downshift in employment might begin around the middle of the year and gain traction over the summer. The June unemployment rate rose to 4.1% while private payrolls ex-education and healthcare (a barometer of cyclical employment) rose just 54,000, far below the previous 6-month average of 101,000. In the second quarter, consumer spending also slowed, rising at a less than 2.0% annualized rate or close to half the 2023 rate.

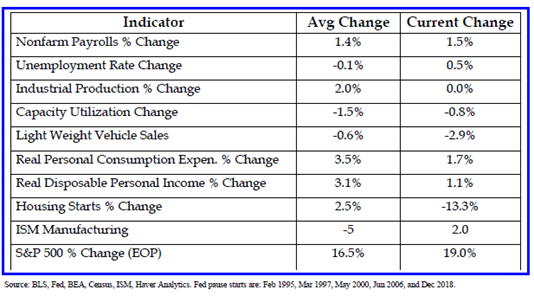

The table below illustrates how current economic data compare to data during past Fed pauses. A Fed pause is defined as the time between the last interest rate hike and the first cut. Most data points are weaker than during past Fed pauses, suggesting the economy is cooling at a faster pace. Now that inflation has resumed moving towards the Fed’s target, the Fed should begin easing monetary policy, or at least begin telegraphing interest rate cuts to let the bond market begin to do the work for them. The sooner, the better-before the water freezes. Chairman Powell, who had previously focused more on inflation during his speeches, has recently started to emphasize employment. During his recent semi-annual Monetary Policy Testimony, Powell stated “elevated inflation is not the only risk we face.” It wouldn’t surprise us to see several interest rate cuts later this year.

Revisiting our previous discussion on economic landings, how might the plane land? A soft landing is still a possibility. If the Fed eases policy soon, before the water freezes, growth may continue to slow, but the economy may avoid a more serious downturn. Equities may continue to do well in that environment, and perhaps with increased breadth as smaller companies begin to feel some relief from a lower cost of capital. If the Fed is too patient, the economy, like the water, may freeze, increasing the odds of a recession later this year. Chairman Powell appears to recognize this, recently stating “reducing policy restraint too late or too little could unduly weaken economic activity and employment.”

The second half of 2024 is likely to be a bumpier ride than the first half. We remind readers that corrections, defined as equity market declines of 10% or more, occur more frequently than you would think. They typically represent a healthy reset for markets.

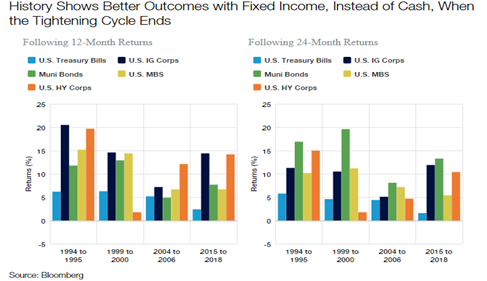

The outlook for bonds appears bright regardless of the ultimate landing. Slowing growth and falling inflation should provide a positive backdrop for total return. While emphasizing ultra short-term bonds has been a good strategy as the Fed aggressively hiked interest rates (an approach referred to as “T-Bill and Chill”), we believe the baton has been passed to intermediate and longer duration bonds. Historically, once the Fed has paused, bonds with longer maturities have outperformed cash both leading up to and during an easing cycle. The volatility around the inflation outlook may have delayed this outcome during the current cycle, but we believe it has started.

The 2024 Election and its Implications

We will dedicate more time to discussing the potential economic and market ramifications of the 2024 election in next quarter’s commentary, which will be sent out just two to three weeks before the election. This election cycle has been unique in several respects. The earlier debate and more recent events may have essentially pulled forward the volatility normally witnessed closer to elections. Additionally, markets may factor in the outcome and its implications over a longer time period.

Portfolio Strategy

During the third quarter we will realign our fixed income strategy to realize several objectives. First, the changes will increase portfolio diversification and allow us to take advantage of additional sectors of the fixed income market that still provide historically attractive yields. Second, we will reduce our exposure to municipal bonds in taxable portfolios while emphasizing intermediate-term maturities to capture better tax-equivalent yields. Third, the realignment includes allocating to both broad-based bond index funds/ETFs and active bond managers with greater opportunity sets and strong performance track records. These changes will also slightly reduce overall portfolio expenses. What won’t change is our emphasis on high-quality, investment grade fixed income investments with a target weighted average duration of under 4 years.

Furthermore, later in the quarter, we plan to implement the new portfolio reporting structure that separates diversifying assets into their own asset class. We will communicate more details about this change shortly before it occurs.

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,