Sun, October 15, 2023

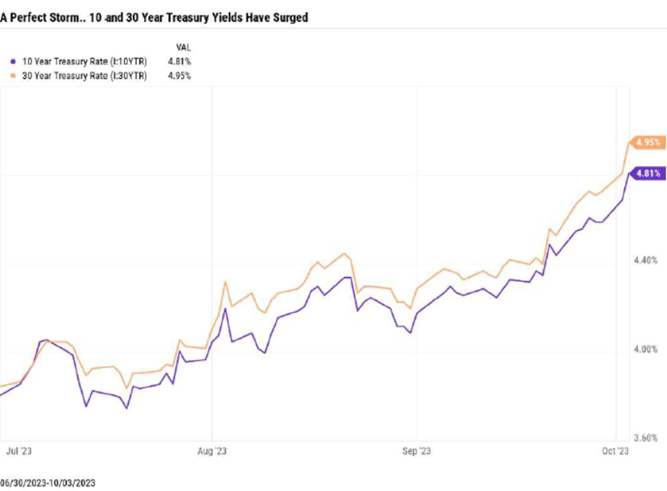

In October 1991, three weather systems converged off the coast of Nova Scotia. The severe event that resulted from this rare combination was chronicled in a 1997 book by Sebastian Junger and ultimately in a feature film adaptation. Since the movie’s release, the term “perfect storm” has entered the popular lexicon, referring to any challenging period that results from the simultaneous occurrence of several negative or unpredictable factors. The US Treasury bond market may be experiencing an event akin to a perfect storm. The convergence of several factors has caused a dramatic rise in yields over the last several weeks, especially in longer-dated treasury bonds. The yield on the 10-year treasury bond has jumped nearly a full percentage point since the end of the second quarter while the 30-year yield has risen just over 1%. We’ll examine three factors-the Federal Reserve’s “higher for longer” message, ballooning government debt and deficits, and quantitative tightening. Furthermore, we’ll discuss the ramifications for the economy, markets, and portfolio strategy.

Higher For Longer

The recent Federal Open Market Committee (FOMC) decision to pause hiking rates did not surprise markets nor did leaving open the possibility of an additional hike in 2023. The real jolt came with the Committee’s forecasts for 2024. The FOMC removed two interest rate cuts from its 2024 projections. Their message suggested a high bar even for those cuts. Despite widespread signs of disinflation, the Fed is concerned that recent economic resilience will stall this process or worse usher in a dreaded second wave of inflation. Of their two mandates, full employment and price stability, the Fed appears to be more focused on the latter. They may not ease policy if the labor market softens unless it’s accompanied by lower inflation and conversely would respond to higher inflation with more hikes regardless of the direction of unemployment.

Fiscal Deficit and Debt

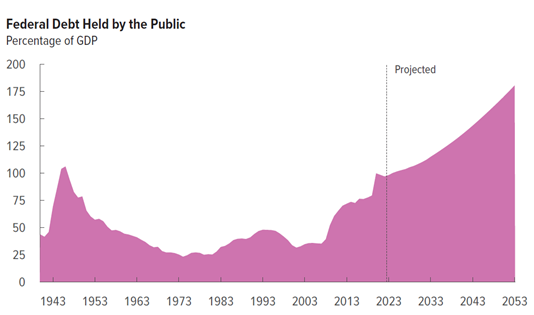

Certainly, our fiscal challenges are not a well-kept secret. While stimulative fiscal policy has arguably helped the economy remain resilient in the face of higher interest rates, total public debt is now about 100% of GDP. The greater supply of debt needed to finance future deficits plus higher financing costs may be leading treasury bond investors to require a higher premium. The CBO estimates that net financing costs will increase from $663 billion this year to $745 billion next year. The dysfunction in Washington certainly doesn’t help sentiment in this regard.

Quantitative Tightening (QT)

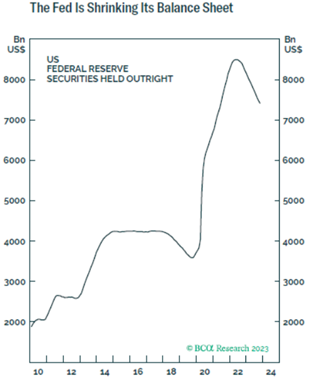

A simple way to understand QT is that the US Treasury market has lost one of its biggest customers. Since the Great Financial Crisis (with a brief pause a few years ago), the Federal Reserve had engaged in quantitative easing (QE). During this period, the Fed was a large and consistent buyer of treasury and mortgage-backed bonds. The goals of QE were to improve liquidity, keep rates low, and stimulate economic activity. However, last June the Fed began QT, stepping out of the market and letting maturing bonds roll off its balance sheet. While QT’s effect on interest rates is harder to estimate, it has contributed to higher volatility and reduced liquidity in the treasury bond market.

Implications

The US economy continues to show resilience and exceed expectations. Economic growth accelerated in the third quarter. September job growth surprised to the upside after cooling for several months. These developments should underpin corporate earnings which will likely resume positive growth after declining for several quarters.

However, looking into 2024, we would be surprised if the surge in borrowing costs didn’t begin to adversely affect the economy. Consumers will feel the squeeze of even higher rates on mortgages, credit cards, and personal loans. Additionally, 36% of banks reported tightening lending standards in the third quarter, a level consistent with past economic downturns. Both the higher cost and reduced availability of credit may begin to play a greater role over the coming quarters.

Moreover, specific tailwinds that have helped soften the effects of higher rates and tighter credit conditions may begin to recede. Stimulative fiscal policy should continue to underpin economic growth but at a diminishing rate. Excess consumer savings built up after the pandemic are still healthy but declining each month. Furthermore, student loan payments have restarted with recent data suggesting an early effect on consumer spending.

Asset Class Performance Review

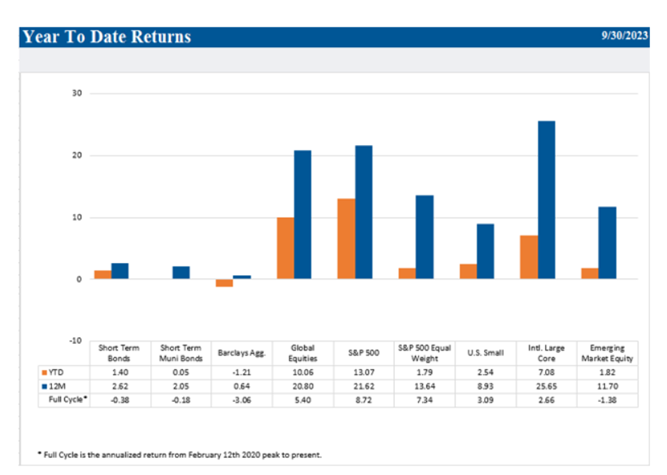

The volatility in the bond market caused global equities to finish the third quarter on a down note. The Russell 3000, a broad index of US stocks, fell 3.3% during the quarter with the bulk of the decline occurring in the second half of September. Developed international and emerging markets declined slightly more than the US as the strong US dollar was an additional headwind. Within the US market, value stocks performed better than growth stocks, but larger companies continued to outpace mid and small-sized companies. In fact, while the market-cap weighted S&P 500 advanced 13% during the first half of the year, an equal-weighted version (which assigns similar weightings to all companies in the index) rose just under 2%.

Fixed income returns were mixed. Long-term bonds suffered negative returns while short-term bonds fared better as high yields offset more modest price declines. However, diversifying strategies were a relative bright spot during the quarter. Most strategies delivered positive returns for the quarter. Reinsurance performed particularly well as it benefited from robust premium income and a benign hurricane season. As we have noted previously, we believe non-correlated strategies will continue to provide valuable diversification benefits.

Portfolio Positioning

Equity: A Further Quality Upgrade

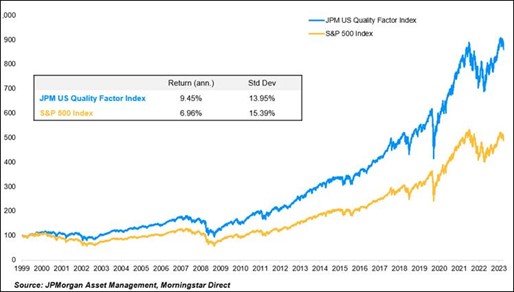

During the quarter, we reduced your allocation to emerging markets, primarily due to our cautious view on China. China faces several structural challenges related to leverage, excess savings, deflation in the property sector, high youth unemployment, and a lack of consumer confidence. We invested the proceeds in a US large-company stock fund that targets companies with high levels of profitability, low leverage, and superior earnings quality. Quality companies with consistent earnings and low debt levels have always been the strategic core of our equity portfolios, but we believe they are especially attractive now given a more uncertain economic outlook. Additionally, quality companies have historically delivered competitive relative returns, especially during the periods following a hiking cycle. Furthermore, the fund is very tax-efficient with low expenses.

Fixed Income: An Expanded Opportunity Set

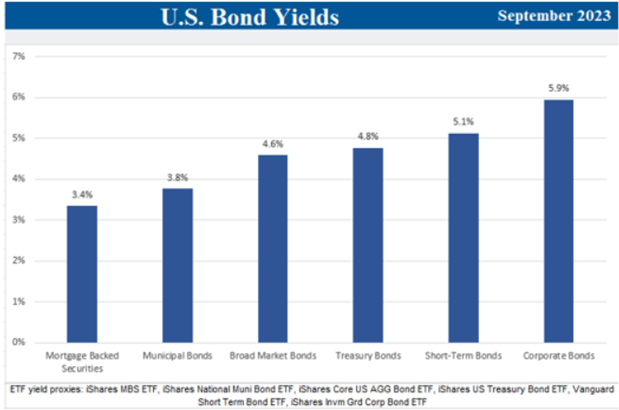

As the fixed income storm passes, it will likely create compelling opportunities. More specifically, bonds in the intermediate part of the curve (often referred to as the “belly” of the curve) are beginning to offer more attractive total return prospects than short maturities. Over the last several weeks, the yield curve has re-steepened dramatically. While short-term (3 years or less) yields have remained steady, intermediate-term yields (3-7 year range) have increased significantly. These bonds now require less of a sacrifice in yield relative to short-term bonds and may also provide better total returns if the economy weakens and inflation continues to decline. Furthermore, similar to high quality companies, the period at or near the end of a Fed hiking cycle has historically been a good time to increase exposure to intermediate bonds.

Diversifying (Non-Traditional) Assets

We have selectively added diversifying assets such as insurance-linked securities, real assets (infrastructure, farmland and timberland), private investment real estate and private lending/credit funds to larger portfolios over the past few years. We expect diversifying strategies to deliver long-term returns between fixed income and global equities, exhibit low correlations to each asset class and thereby reduce overall portfolio volatility. Thus, unique and well-managed strategies are always on our shopping list! We are currently evaluating another compelling opportunity in this space that we may include in client portfolios early next year.

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,