Mon, June 22, 2026

Stocks advanced across the globe led by a rally in semiconductor stocks and a continued decline in oil prices. The U.S. and Iran agreed to a memorandum of understanding, which calls for both Iran to reopen the Strait of Hormuz to pre-war levels and the U.S. to lift its blockade within 30 days. Additionally, the MOU establishes a 60-day timeline to negotiate a final agreement.

Economic Data

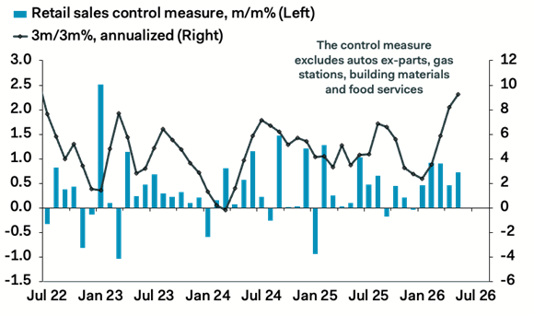

Retail Sales

May retail sales showed few signs of a slowdown in consumer spending. Control retail sales, which exclude more volatile categories such as gasoline sales, rose +0.7% and exceeded expectations for +0.4% growth. The annualized rate of growth in the three months to May rose to 9.2%, the highest since June 2022. Consumption is now tracking at a quarter-on-quarter annualized pace of 2.5%, up from 1.4% in Q1. May was likely the last month in which tax refunds provided a material tailwind.

FOMC Meeting

There were two main takeaways from the Federal Open Market Committee’s (FOMC) meeting and Federal Reserve Chair Kevin Warsh’s first press conference. First, the Fed now has a hiking bias. Nine of the eighteen meeting participants project one or more 0.25% rate increases this year. Eight expect the policy rate to remain unchanged, while one participant projected a cut. The Fed also raised its estimate of 2026 core inflation from 2.7% to 3.3%. Additionally, the sentence “The Committee will deliver price stability” was emphasized by Warsh repeatedly during the press conference.

Second, the FOMC did not include any forward guidance in its rate policy statement. In fact, the statement was the shortest since 2007. This shouldn’t have been surprising given Warsh’s past criticism of forward guidance, a view he reiterated during his recent nomination process. Still, the terseness of the statement appeared to catch investors off guard. We can expect less forecasting or projections from the Fed going forward. Warsh has also established five task forces, each dedicated to evaluating potential changes in how the Fed communicates and conducts policy.

Our Take

The Fed has transitioned from an easing bias as recently as March, to a “thinking about hiking rates” bias in May, to a hiking bias currently. As we pointed out recently, the increasing gap between the 2-year Treasury yield and the federal funds rate suggested the Fed was behind the curve. Certainly, the effects of the war with Iran have carried some weight, although those headwinds should recede over the next several months. However, better-than-expected economic growth has been the other factor.

If economic growth remains resilient and above potential, the Fed may begin raising interest rates. We believe one key variable is wage growth. Wage growth has moderated over the last few months. Should wage pressure resume, the Fed may need to begin tightening.

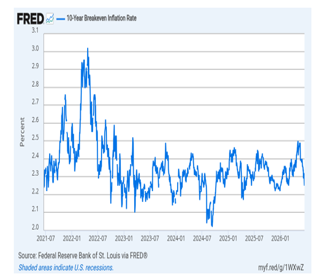

The good news is long-term inflation expectations remain anchored and have drifted lower with the recent decline in oil and other commodity prices. According to the Federal Reserve Bank of St. Louis, the 5-year and 10-year breakeven inflation rates (the difference in yield between a nominal treasury and a treasury inflation-protected bond of the same maturity) are 2.27% and 2.25% respectively.

Moreover, the 2-year breakeven inflation rate has fallen to 2.2%, below the level before the war again. Regardless, in the near term, higher bond volatility (at least on the short end) is possible given a regime of less communication, forecasting, and guidance.

Markets

U.S. Equities

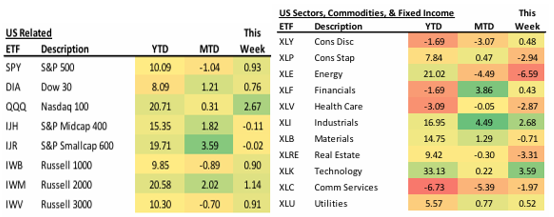

U.S. stocks initially swooned after the FOMC statement and Warsh’s press conference. They rebounded Thursday, and the S&P 500 closed the week with a nearly 1% gain. Small caps advanced just over 1%. The semiconductor rally was in full force and accounted for the lion’s share of gains in the technology sector. Industrial stocks, particularly those more exposed to the AI infrastructure buildout, also performed well on a relative basis. Overall, market breadth contracted. Five of the ten S&P 500 sectors declined 2% or more for the week.

International Equities

Japan’s Nikkei 225 surged to a new record. In May, Japanese exports grew 17% year-over-year, the fastest pace since November 2022. Japan has benefitted from the global AI boom (semiconductor exports grew 61.2%), although the weak yen has certainly helped. Export volumes grew just 0.5%, suggesting much of the growth came from price increases and foreign exchange impacts. The yen is approaching a four-decade low relative to the U.S. dollar. This decline may trigger another round of intervention from the Bank of Japan. Emerging markets also had a strong week led by a renewed rally in semiconductor stocks.

Fixed Income

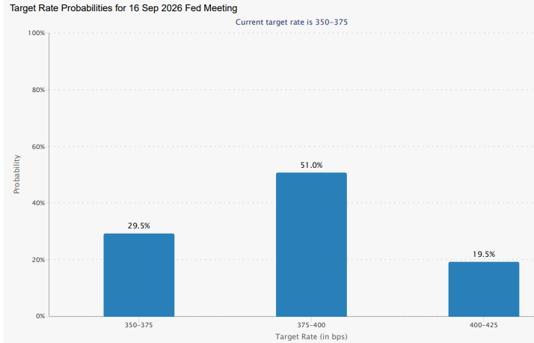

The 2-year Treasury yield spiked after the FOMC meeting (+14 basis points), further flattening the Treasury curve. The 2-year/10-year spread has declined from over 70 basis points earlier in the year to around 25 basis points currently. Fed funds futures are pricing in a 70% probability of one to two interest rates hikes by September. Credit spreads have remained benign, holding near their tightest levels.

This Week

Economic data includes May personal income and spending, Q1 GDP revision, and Core PCE.

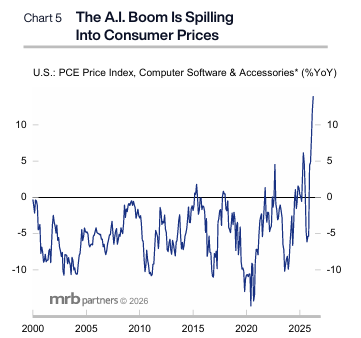

Chart of the Week

Is AI inflationary or disinflationary? Arguably, the potential long-term benefits of AI (higher productivity) are disinflationary. However, in the near term, the AI capex boom may be spilling into higher consumer prices. Last week, Apple stated they will raise prices due to soaring memory costs.

Written By Brian Presti

--

Brian Presti, CFA®, Chartered SRI Counselor℠, is Chief Investment Officer and a shareholder at TFC Financial Management. He oversees the firm’s investment strategy, asset allocation, and portfolio management processes and leads the firm’s Investment Committee. Brian specializes in portfolio construction, capital markets analysis, and sustainable and responsible investing. As CIO, he is responsible for evaluating investment managers and implementing portfolio strategies designed to support long-term client objectives.