Mon, June 15, 2026

Despite significant volatility, equities advanced on the back of lower oil prices and bond yields. SpaceX had a strong showing during its first day of trading. Over the weekend, it appeared the U.S. and Iran are the closest they have been to an agreement to end the war and reopen the Strait of Hormuz.

Economic Data

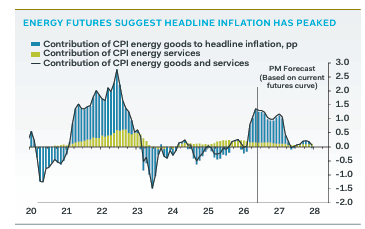

CPI: Headline CPI rose 0.5% month-over-month and 4.2% year-over-year. The increase was primarily caused by an additional 7% rise in gasoline prices. However, if oil prices track the path implied by futures markets, May will likely mark the peak effect. Moreover, other components of inflation remain stable. For example, the 0.29% monthly rise in core services prices matched the average pace of the last six months. Core CPI (ex-food and energy) rose 0.2% in May and 2.9% over the last 12 months.

PPI: The PPI report showed building goods price pressures. Headline PPI rose 1.1% in May, pushing the annual rate to 6.5%, the highest since November of 2022. Combining May CPI and PPI leads to an estimated 0.38% increase in the May core PCE deflator (the Fed’s preferred gauge), lifting inflation to 3.4% from 3.3% in April. The core PCE deflator will likely remain 3%+ over the summer and keep the Fed on the sidelines at the very least.

Jobless claims: While the absolute level of weekly initial jobless claims (229k) is still very low, the four-week average has crept up to the highest since February. The trend in the leading indicators of claims (Challenger job cuts, WARN notices) remains flat.

Markets

U.S. Equities

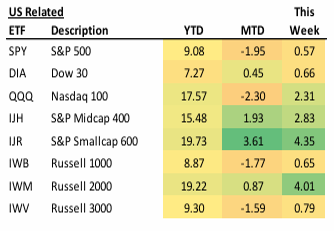

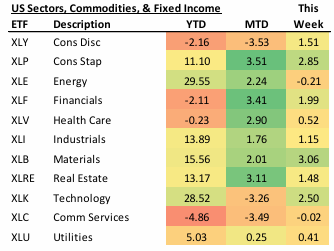

The expansion in market breadth that began two weeks ago continued in earnest last week. The S&P 500 rose 0.7% while the financials, materials, consumer staples, real estate, and consumer discretionary sectors all at least doubled that return. However, the star of the show last week was small companies. The Russell 2000 index surged 4% and eclipsed its all-time high from late May. The equal-weighted S&P 500 also reached a new high and is now outpacing the market-cap weighted S&P 500 year to date.

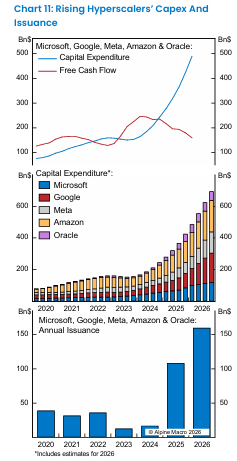

Within technology, stock performance has continued to show significant dispersion. Semis bounced back and resumed their leadership position within the sector. Conversely, hyperscalers such as Meta and Microsoft have lagged as investors remain skeptical about whether hyperscalers’ massive AI capex will translate to adequate returns on investment. Investors have been particularly cautious towards those companies who have raised capex budgets and/or are issuing large amounts of debt or equity to fund capex.

International Equities

Profit taking in semiconductor stocks hit emerging markets early in the week, although they bounced back to finish essentially flat for the week. Developed markets advanced with strength in select markets such as southern Europe and Australia. Japan’s Nikkei surged 5% overnight on the back of U.S./Iran deal optimism.

Fixed Income

Despite the inflation data, Treasury yields declined across the curve. Yields have largely tracked oil prices which fell to their lowest levels since April. As we mentioned earlier, May could mark the peak effect of gasoline prices on CPI. According to AAA, the national average for a gallon of regular gas has fallen from $4.56 on May 21 to $4.07 on June 14.

This Week

The Federal Open Market Committee will meet on Tuesday and Wednesday. Investors will focus on Kevin Warsh’s first press conference as Fed Chair. The most important economic data is May retail sales which will be released on Wednesday morning.

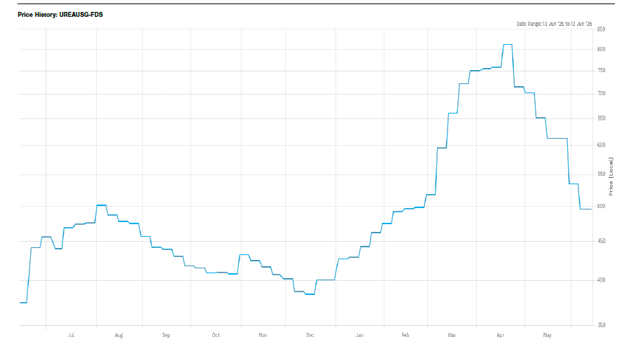

Chart of the Week

In addition to the recent decline in oil prices, urea prices have plummeted and are back to their pre-war levels. Urea is an important agricultural input and is widely used in fertilizers as a source of nitrogen.

Written By Brian Presti

--

Brian Presti, CFA®, Chartered SRI Counselor℠, is Chief Investment Officer and a shareholder at TFC Financial Management. He oversees the firm’s investment strategy, asset allocation, and portfolio management processes and leads the firm’s Investment Committee. Brian specializes in portfolio construction, capital markets analysis, and sustainable and responsible investing. As CIO, he is responsible for evaluating investment managers and implementing portfolio strategies designed to support long-term client objectives.