Wed, April 15, 2026

When we mentioned “policy overreach with unintended consequences” as a risk for 2026, a war with Iran was not our base case. We believe the economy and corporate earnings entered this shock from a position of strength, but investors may need to navigate a shifting growth landscape depending on the duration of the war and the magnitude of its effects.

State of the Global Economy and Corporate Earnings

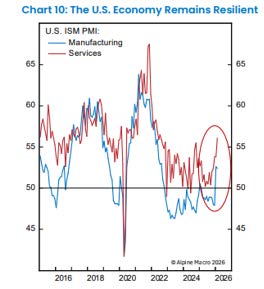

The U.S. economy started 2026 in good shape. Recent indicators suggest an underlying momentum supported by pro-growth fiscal and regulatory policy, productivity gains, and capital investment. For the first time in several years, both the Manufacturing and Services Purchasing Managers Indices’ are in expansion territory.

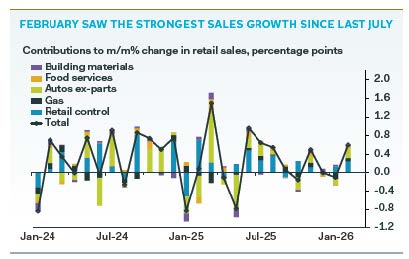

February retail sales showed the best growth since last July.

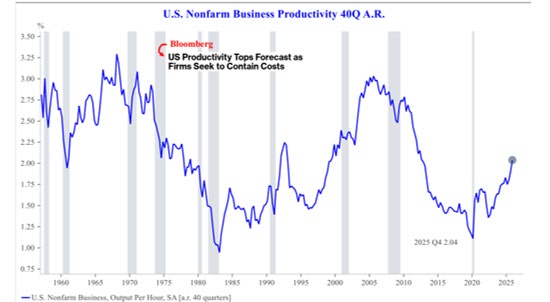

Productivity growth is rising, helping to mitigate cost pressures and expand margins.

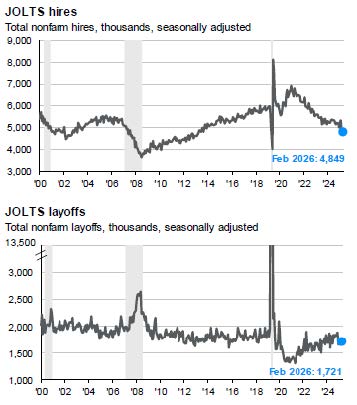

Admittedly, the employment outlook has been mixed. The labor market bounced back in March, although we would downplay the strength (as we would the weakness in the February report). The “little hiring, little firing” trend of the last several months appears intact.

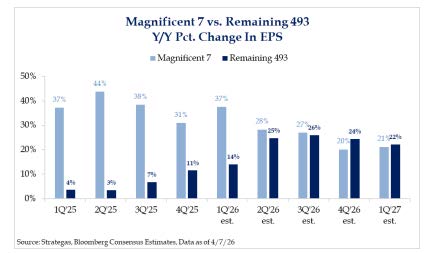

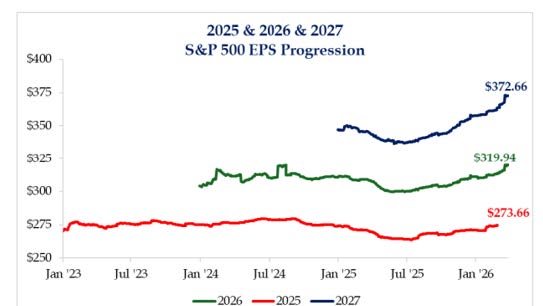

Furthermore, corporate earnings growth has been strong. S&P 500 earnings grew 12% in 2025 and are expected to accelerate to 17% in 2026. Profit margins are at records and close to levels few predicted 12 months ago. Moreover, earnings growth is broadening. Technology should continue to carry the lion’s share given its large weighting, but relative earnings growth has picked up in more cyclical sectors such as industrials and financials. Earnings growth should also improve further down the capitalization spectrum as 2026 progresses. These trends likely reflect the supportive policy tailwinds we have discussed in past commentaries.

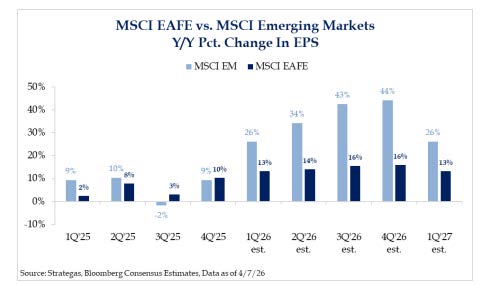

Overseas, many developed and emerging market economies are also benefitting from policy tailwinds and delivering strong earnings growth.

The key question going forward is to what degree will the war affect this underlying economic and earnings momentum?

The War: Immediate Effects, Key Unknowns, and Potential Implications

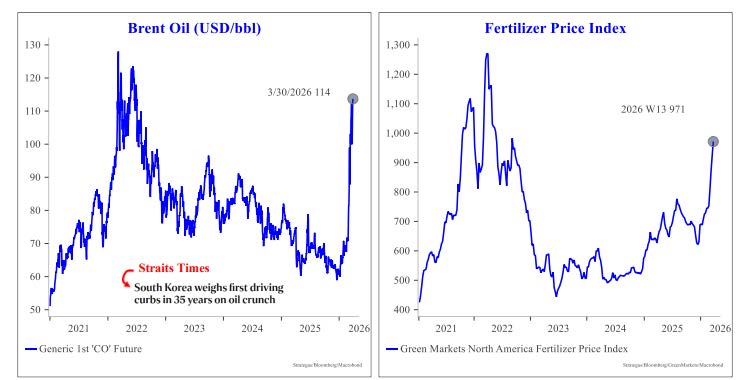

The most immediate effect of the war has been a global commodity supply chain shock. In addition to oil, the following supply chains have been disrupted:

- Natural gas

- Refined products (e.g. gasoline)

- Fertilizer and inputs

- Aluminum

- Helium (important input for technology)

- Naphtha (petrochemical inputs)

- Plastics inputs

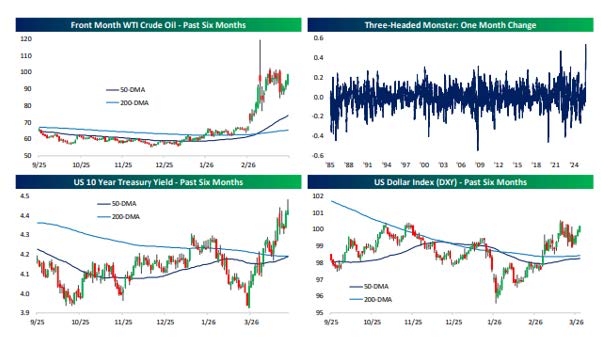

Additionally, financial conditions have tightened, although they have eased recently. The “three-headed monster” index (oil, the U.S. dollar, and the 10-year yield) rose by the largest amount ever in March.

Short-term inflation expectations have spiked. Medium to long-term expectations have remained benign. Expectations for monetary policy have shifted, especially outside the U.S. where most central banks are governed by a single mandate of price stability.

The key unknowns going forward are:

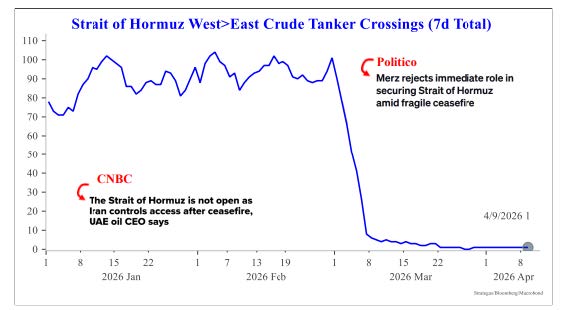

- Duration of the effective closure of the Strait of Hormuz

- The ultimate level of energy (and other commodity) prices

- The length of time energy/commodity prices remain elevated

- The extent and duration of supply chain disruptions

Obviously, we can’t predict when the war will end. However, we can reasonably make two assumptions. First, the longer the war drags on, the greater the economic effects will be, especially if financial conditions tighten further. Second, even if the war ends soon, there will be economic spillover. The magnitude is difficult to estimate at this point. If traffic through the Strait of Hormuz improves, it will likely take some time to reach pre-war levels. Additionally, numerous oil fields, refineries, pipelines, and other energy infrastructure in the Middle East have been severely damaged or impaired. The International Energy Agency recently stated that 40 energy assets across nine countries have been destroyed.

The magnitude and duration of supply chain disruptions and the length of time energy and other commodity prices remain elevated are key unknowns that have implications for the global economy.

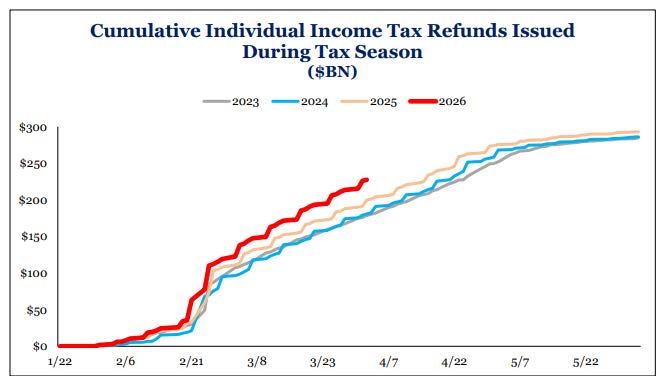

We do not expect the war to cause a global recession, but the spillover will dampen growth relative to pre-war expectations. The U.S. economy should be more resilient given its lower sensitivity to energy prices and underlying policy support. However, to an extent policy may now act as more of a shock absorber than a growth contributor. For example, due to OBBBA consumer tax refunds are up over 10% relative to last year. A portion of these refunds may be redirected towards higher energy costs or kept in savings.

The near-term hit to consumer sentiment and real incomes is significant. The headline index of the most recent U.S. Michigan Consumer Survey plunged to its lowest level on record. While sentiment has not correlated with spending over the last 12 months, any time an economic series achieves a new record, it catches our attention.

Businesses will continue to take advantage of stimulative provisions within OBBBA but may delay new investments due to higher costs and supply chain disruptions. Upcoming corporate earnings reports and company guidance will be very important. Earnings estimates (S&P 500 expected earnings growth of 17% this year) haven’t budged. In fact, they have risen modestly since the war began. Estimates may be reduced during the Q1 reporting season, although the effects of higher costs and supply chain disruptions may take several months to be felt.

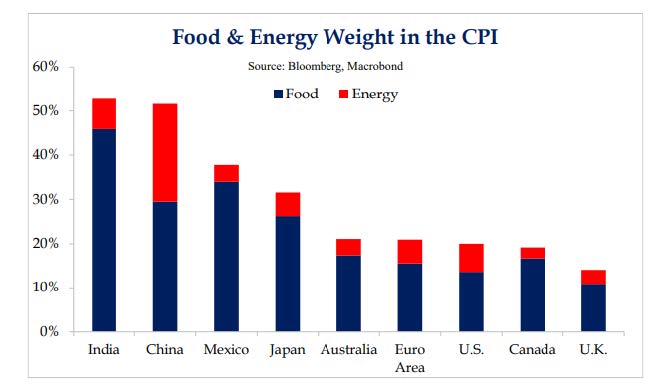

Outside the U.S., international economies may feel the effects of the war to a greater degree. Roughly 20% of global oil consumption transits the Strait of Hormuz. An estimated 80% of this crude oil flows to Asia. European consumers spend roughly three times more of their disposable income on energy than U.S. consumers. Moreover, since the war began interest rates have risen more outside the U.S., especially in Europe. Unlike the Federal Reserve, the European Central Bank does not operate under a dual mandate (full employment and price stability). The ECB’s overriding objective is to focus on price stability, although they may choose to look through temporary supply shocks when calibrating monetary policy.

Asset Class Performance Review

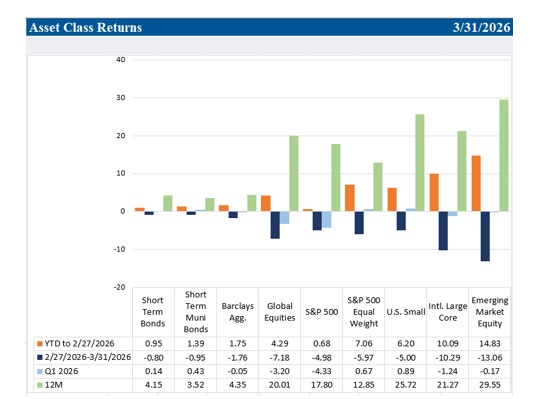

Asset class performance in the first quarter diverged between the pre-war (January and February) and post-war (March) periods. Through February, international equities picked up right where they left off in 2025. Developed and emerging markets gained over 10% and 14% respectively. The broad U.S. market had eked out a minor gain before the war. Bonds rallied early in the year with the 10-year yield reaching 3.95% the day the war started.

Despite the pullback in March, most asset classes ended the quarter close to where they started the year. Additionally, in April both stocks and bonds have recaptured a portion of the recent declines as oil prices retreated from their recent highs. As of the week ending April 10, the S&P 500 had recaptured 75% of its decline, and international markets are now firmly back in positive territory for the year. After nearly reaching 4.5%, the 10-year yield has fallen to 4.3%. Notably, all diversifying assets strategies were positive during the first quarter, reinforcing their valuable role, especially during periods of heightened volatility.

In last quarter’s commentary, one of the themes we highlighted for 2026 was the rotation that began in the U.S. market near the end of the third quarter of 2025. Investors had begun to rotate from mega-cap technology companies (the Mag 7) into value stocks, cyclical sectors, and small to mid-sized companies. We believed this rotation was likely more to be sustainable than it has been in the past given the supportive policy backdrop, broadening earnings growth, and increased investor scrutiny around AI capital expenditures. The rotation has continued this year. The equal weight S&P 500 outpaced the market-cap weighted S&P 500 by 5% in the first quarter. Our U.S. equity strategy is well suited for this environment given our broad diversification across market caps, styles, and sectors. We still maintain this conviction, although we can’t rule out a rotation back into mega-cap technology stocks if investors become concerned about economic growth.

Portfolio Strategy

Our core belief is that globally diversified, multi-asset class portfolios enhance the investment opportunity set and are best suited for a variety of economic and market environments. Prudent diversification increases the likelihood of achieving long-term returns while also mitigating declines during short-term market disruptions. Diversification proved to be valuable during the first quarter, and we believe it will continue to be going forward.

Additionally, we are also mindful of the importance of periodic portfolio rebalancing. During the quarter, portfolios that were significantly overweight equities were rebalanced back to their target allocations while adding to fixed income or cash reserves, where appropriate. We also swapped a more concentrated, higher beta (risk) small company growth fund into a broadly diversified, lower cost index option. This move will lower expenses and may enhance returns.

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,

--

Brian Presti, CFA®, Chartered SRI Counselor℠, is Chief Investment Officer and a shareholder at TFC Financial Management. He oversees the firm’s investment strategy, asset allocation, and portfolio management processes and leads the firm’s Investment Committee. Brian specializes in portfolio construction, capital markets analysis, and sustainable and responsible investing. As CIO, he is responsible for evaluating investment managers and implementing portfolio strategies designed to support long-term client objectives.

Renée Kwok, CFP®, is President and CEO of TFC Financial Management, a fee-only registered investment advisor providing comprehensive financial planning and wealth management services. She has over three decades of experience advising individuals and families on investment strategy, retirement planning, tax planning, and multi-generational wealth management. Renée joined TFC Financial in 1991 and leads the firm’s financial planning and investment advisory services while serving on the firm’s Investment Committee. Prior to TFC, she worked as a security analyst at Putnam Investments and as an investment analyst at Asian Oceanic Limited, a Hong Kong merchant bank.