Thu, January 15, 2026

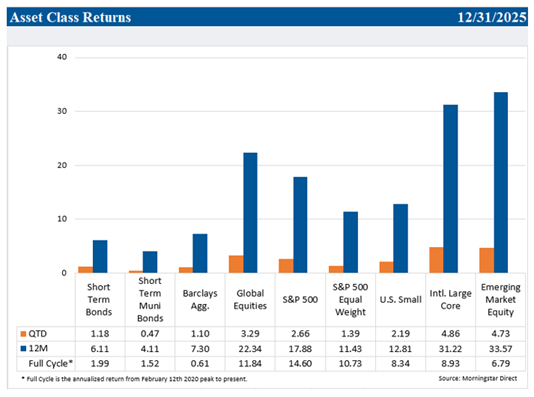

While it may have appeared unlikely in the throes of post-Liberation day volatility, 2025 ended up being a very fruitful year for investors. Each major asset class delivered a historically above average return. Global equities rose over 20%, led by international equities which had their best year since 2009. 2025 was the first year since 2017 that both international developed and emerging market equities outperformed U.S. equities, although the latter still provided strong returns. Yields declined and credit conditions remained benign which contributed to the best total returns in fixed income since 2020.

Asset Class Performance Review

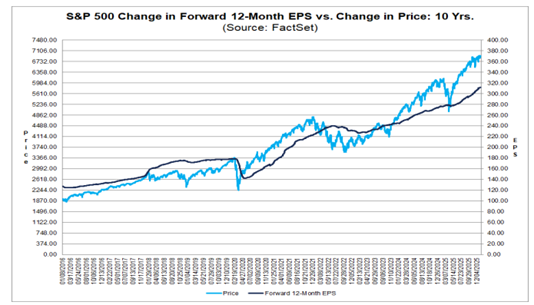

If we had to choose the single most important factor for equity market performance, we’d point to corporate earnings growth. U.S. stocks were supported by strong profit growth-in both absolute and relative terms. Earnings growth in 2025 may exceed 10% and easily surpassed expectations each of the first three quarters (4th quarter earnings season just began). This trend is expected to continue in 2026. Earnings growth is estimated to accelerate to near 15% year-over-year. Moreover, profit growth should broaden this year due in part to the supportive pro-growth policy mix we discuss below.

Strong profit growth was not just a U.S. story. Financial and industrial stocks led earnings growth in developed markets while technology carried the torch within emerging markets. International markets were also buoyed by a weak U.S. dollar (the worst year for the greenback since 2017), easier monetary policy, and the prospects for fiscal stimulus.

As we look forward to 2026, we believe there are several themes that may dictate economic and market performance.

Theme #1-More policy “ice cream” ahead of the midterms

In last quarter’s commentary, and during our November webinar, we discussed how the “spinach” of tariffs and government austerity was gradually offset by the “ice cream” of pro-growth fiscal, monetary, and regulatory policy. Moreover, the fact that pro-growth policies are aligned while the economy and corporate profits are expanding is unusual. Pro-cyclical policies normally arise during downturns or recessions.

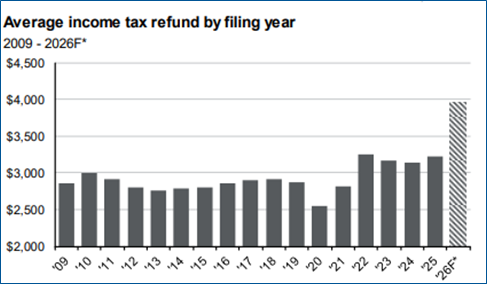

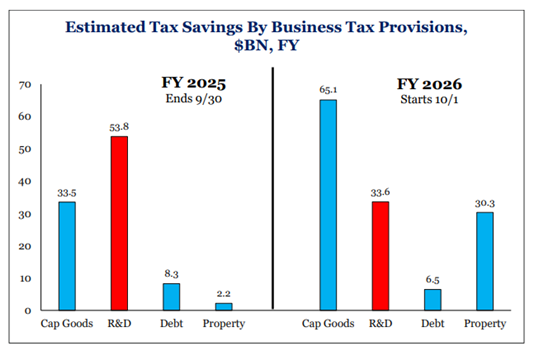

Fiscal policy provided support for businesses in 2025 through various stimulative provisions in the OBBBA. Examples include the immediate expensing of building factories and production facilities, accelerated depreciation, expensing of R&D costs, and higher deductibility for interest expense. Estimated tax savings are expected to accelerate in 2026. Consumer stimulus will hit early this year and may result in an estimated $150bn of additional tax refunds. Regarding monetary policy, the Federal Reserve lowered rates by 0.75%, and after a pause in January may resume cutting rates in March. Importantly, the Federal Reserve is lowering rates while expanding its balance sheet.

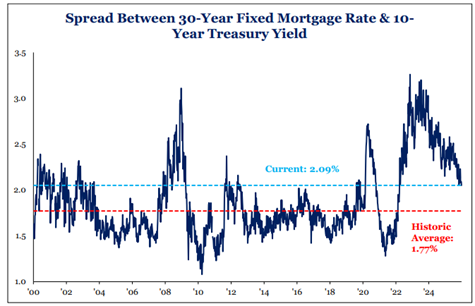

However, in 2026 we believe the “ice cream” will be served on the regulatory front. More specifically, the administration will likely pull several regulatory levers to revive the stagnant housing sector. The primary objective is to lower mortgage rates. Reducing mortgage rates may be accomplished by keeping the general level of interest rates low but also by narrowing the spread between the 10-year treasury yield and mortgage rates. This spread has been historically high over the last few years, although it has been declining recently.

The administration will aim to use deregulation to free up excess bank capital to buy Treasuries and Mortgage-Backed Securities (MBS). Additionally, on January 8th, President Trump directed the GSEs (Government-Sponsored Enterprises such as Fannie Mae, Freddie Mac, and the Federal Home Loan Banks) to increase their mortgage purchases by $200bn. Recently, Treasury Secretary Scott Bessent stated the “only missing ingredient” for a stronger economy is lower interest rates. Other levers include selling federal land for housing, assuming FHA mortgage rates, mortgage portability, and allowing penalty-free 401k withdrawals for down payments.

It appears the administration’s objective is a “run it hot” economy that grows above trend, especially ahead of the mid-term elections.

Theme #2-Productivity Boom

In last quarter’s commentary, we discussed how productivity growth was an important factor contributing to corporate profit growth. Historically, the economy has experienced distinct phases of productivity growth that can last years, if not decades. These periods typically coincide with important technological advancements. We may be in the early phase of a multi-year upturn after a long period of anemic growth; nonfarm productivity surged in Q3 at a 4.9% annual rate. A.I. is likely a factor, but it’s not the only reason. A post-pandemic surge in new business formation, shifting work models, and supply chain optimization are also contributing.

While the excitement around a new technology is initially directed towards the enablers (e.g. railroad companies in the 1800s, telecomm equipment makers in the late 1990s and cloud providers/semiconductors currently), productivity and efficiency gains ultimately accrue to the adopters. For example, recent comments from banking executives suggest A.I. is leading to efficiencies in fraud detection, credit risk assessment, and automating routine tasks. Healthcare companies have pointed out benefits for drug discovery and diagnostics while industrial companies have cited automation.

Theme #3-A more sustainable market rotation….finally

The multi-year outperformance of mega-cap technology stocks relative to the broader market has been well publicized. Last quarter we dedicated a fair amount of space to discussing the risks of excessive market concentration, especially in light of the increasing operating leverage several large tech companies were taking on to fund capital expenditures related to AI.

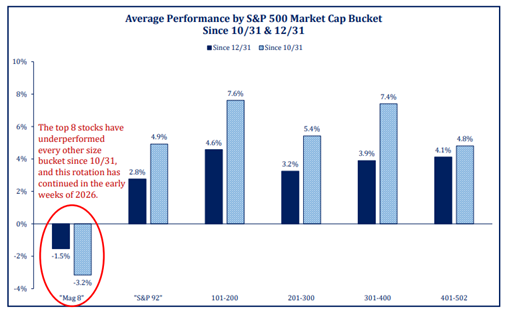

During Q4, and especially since late October (notably after Nvidia’s last earnings report), market breadth has improved considerably. In other words, more sectors and market capitalizations have participated in the market’s advance. While early, 2026 has started off with the same trend.

Sure, we have seen this movie before. Expansions in breadth have been fleeting as the market ultimately drifted back to the familiar Mag 7 names. What is unique about this environment? First, we’d point to the two themes we just discussed. The policy mix should lead to broader profit growth. Fiscal policy will likely benefit more cyclical sectors such as industrial and manufacturing companies and may also help smaller companies. Moreover, small company earnings should have higher sensitivity to lower rates. Deregulation should increase bank profitability through a steep yield curve and increased M&A. Productivity growth may become more broad-based.

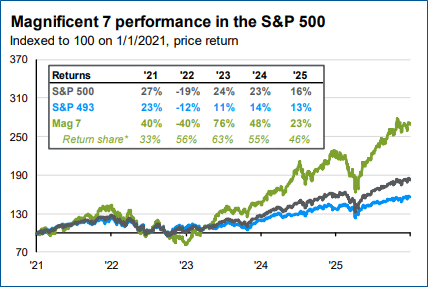

Second, performance within mega-cap technology has become increasingly bifurcated as investors become more discerning about capex spending, leverage and future profitability. This may lead to less of a rising tide lifts all boats approach to the AI names. The contribution of the Mag7 stocks to the S&P 500 return decelerated from 63% in 2023 to 55% in 2024 to 46% in 2025 with just two of the Mag 7 outperforming the S&P 500 last year.

Lastly, we find it encouraging that despite several Mag 7 stocks trading significantly below their 52-week highs, the overall market is not far off the same level. Capital is not fleeing the market but rather rotating within it given the sound underpinnings we discussed previously.

Theme #4-The heavy hand of Washington

The Trump administration has started the year with several populist directives and proposals targeting various industries. Trump has taken steps to ban institutional investors from buying single family homes, prohibit defense companies from issuing dividends and engaging in stock buybacks, and cap credit card interest rates at 10%. Electricity price proposals may be next. It’s difficult to determine whether these announcements will translate into actual policy or if they are simply grand gestures in a midterm election year with the issue of affordability front and center. Regardless, more rather than less intervention is likely. Outside of volatility in the sectors most affected, the broad market has taken these proposals in stride so far. However, we should be wary of potential unintended consequences. For example, capping credit card rates and/or restricting investment could offset some of the tailwinds from deregulation. Furthermore, the move could slash credit access for many borrowers.

Similarly, intervention has increased on the geopolitical stage. The “Donroe Doctrine”-asserting U.S. dominance and mitigating outside influence in the Western Hemisphere-may heighten the risk of policy overreach with unintended consequences. Renewed intensification of a trade war (after U.S. businesses likely concluded we had passed peak tariffs) could affect growth and hiring.

Asset Class Performance Review

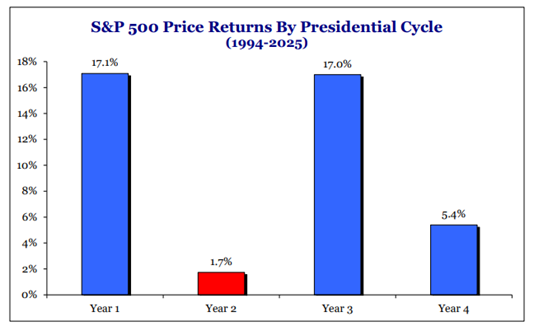

While we maintain a positive outlook, some historical context is important. First, a fourth straight year of double-digit gains could be a challenge. According to Bespoke Investment Group, four straight years of double-digit gains have only occurred in three periods since 1928 (1942-45, 1949-52, and 1995-1998).

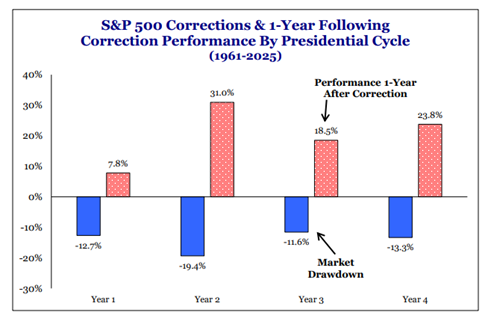

Additionally, midterm election years tend to be the worst year for stocks in the 4-year presidential cycle. Year 2 also tends to have the highest volatility with the largest average drawdowns. We wouldn’t be surprised to see more swings in the market in 2026. This may be a year in which the economy exceeds expectations but equity returns do not.

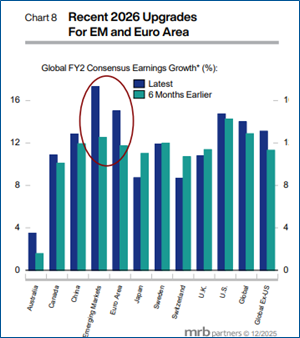

Global equity diversification will continue to be important. Even after last year’s performance, both developed and emerging market equities are attractively valued and have catalysts of their own. The global economic expansion should continue next year, which will benefit non-U.S. earnings in both absolute and relative terms. Furthermore, developed market equities should be less sensitive to any unwinding of the A.I. narrative given their higher exposure to cyclical and value stocks such as financials and industrials. Lastly, fiscal and/or monetary stimulus should support markets, especially in parts of Europe, China, and now Japan.

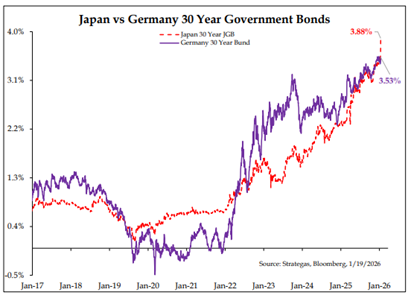

Fixed income volatility has remained low for several months but may increase due to concerns related to Federal Reserve independence. Furthermore, while the administration is using several levers to anchor bond yields, ex-U.S. longer maturity bonds have been rising steadily (especially in Japan). The inertia of global curve steepening may begin to affect U.S. yields. 2026 may end up being a clipping coupons year in which still attractive income yield is the bulk of the return for bond investors. We continue to prioritize diversification and high quality in our fixed income allocations.

Diversifying assets performed well in 2025, providing uncorrelated returns that generally exceeded those of fixed income. We continue to believe they will serve as valuable diversifiers in 2026.

Please contact your TFC Advisor or us directly if you have any questions or would like to discuss your portfolio further. Thank you.

Sincerely,

--

Brian Presti, CFA®, Chartered SRI Counselor℠, is Chief Investment Officer and a shareholder at TFC Financial Management. He oversees the firm’s investment strategy, asset allocation, and portfolio management processes and leads the firm’s Investment Committee. Brian specializes in portfolio construction, capital markets analysis, and sustainable and responsible investing. As CIO, he is responsible for evaluating investment managers and implementing portfolio strategies designed to support long-term client objectives.

Renée Kwok, CFP®, is President and CEO of TFC Financial Management, a fee-only registered investment advisor providing comprehensive financial planning and wealth management services. She has over three decades of experience advising individuals and families on investment strategy, retirement planning, tax planning, and multi-generational wealth management. Renée joined TFC Financial in 1991 and leads the firm’s financial planning and investment advisory services while serving on the firm’s Investment Committee. Prior to TFC, she worked as a security analyst at Putnam Investments and as an investment analyst at Asian Oceanic Limited, a Hong Kong merchant bank.